WEEK ENDING 2/24/2023

Highlights of the week:

- The markets are giving up positive returns for Lent.

- Inflation proves a pesky little bugger.

- A smart reader asked why we haven’t commented on the inversion of the municipal bond yield curve. This week we do.

- A “national divorce”? We’ve done this before.

A CITY DIFFERENT TAKE

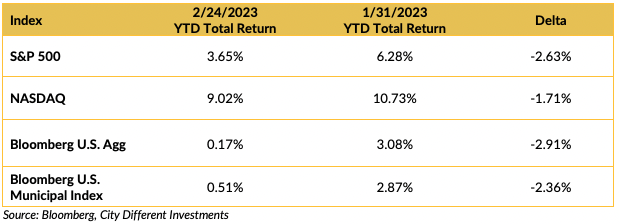

This year’s trend of positive returns seems to have hit a wall in the last couple of weeks as inflation looks to be a pesky bugger.

Fat Tuesday was last week, and it looks like the markets are giving up positive returns for Lent.

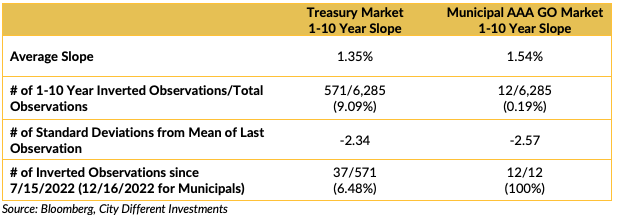

A smart friend of ours pointed out that the municipal index almost never inverts. We agree with that observation and want to add some context to that statement. We have a database that goes back to June 1994, covering several interest rate cycles. (Municipal market data from before 1994 is difficult to come by.)

The inverted yield curve is a rarity, never seen in our careers. Does that change our commitment to the laddered structure of our municipal separately managed accounts? No it does not.

CHANGES IN RATES

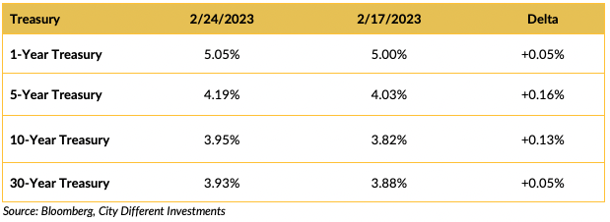

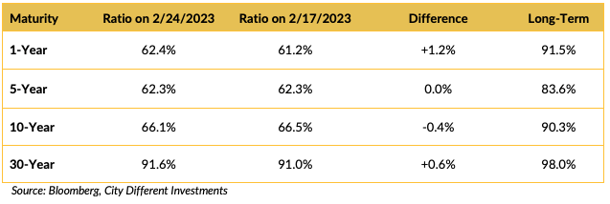

The PCE release was hotter than expected. The year-over-year (Y/Y) headline number came in at 5.4%, above an expected reading of 5%. Last month’s reading was revised from 5% to 5.3%. The Y/Y core PCE release followed the same trend coming in hotter than expected at 4.7% vs. 4.3%; last month’s release was revised from 4.4% to 4.6%. The slope of the 1-to-30-year Treasury curve remained unchanged.

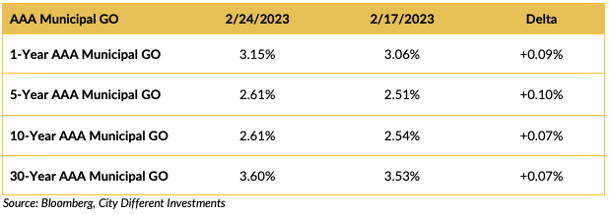

The municipal market followed the Treasury market to higher yields at about the same rate. Last week was a holiday-shortened week with limited new-issue supply. This lent support (no pun intended) to the municipal market.

The above ratios and their weekly changes represent how the two fixed-income markets recorded different reactions.

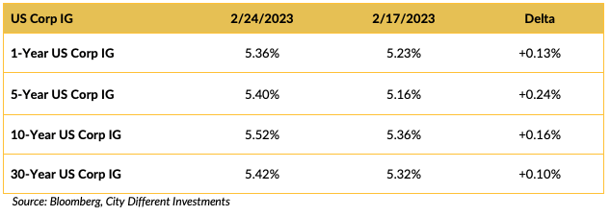

The investment grade (IG) corporate market shared the week's volatility.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

Most of the Washington news this week revolved around Kyiv and President Biden's visit. That was the first time an American president visited a war zone without U.S. troops deployed in that theater — quite a big show of support.

In other Washington news, Rep. Marjorie Taylor Greene called for a “national divorce.”

“We need to separate by red states and blue states and shrink the federal government,” Greene tweeted.

That article references polls showing support for secession,

“A June 2021 poll by Bright Line Watch and YouGov found that 66% of Southern Republicans supported leaving the U.S. and forming a new country. Support was also high among Democrats in the West, where 47% supported a division.”

See what happens when you don’t teach history correctly? We tried this in the 1860s. A financial question came to mind. Since most southern states receive more federal aid than the taxes they pay into the national system, would there be an alimony arrangement between the states if we divorce?

Here is an interesting factoid. Which state claims the greatest difference between federal aid received and federal taxes paid (according to MSNBC)? The answer is Kentucky. That brings back memories of Sen. Mitch McConnell and President Biden in front of a bridge.

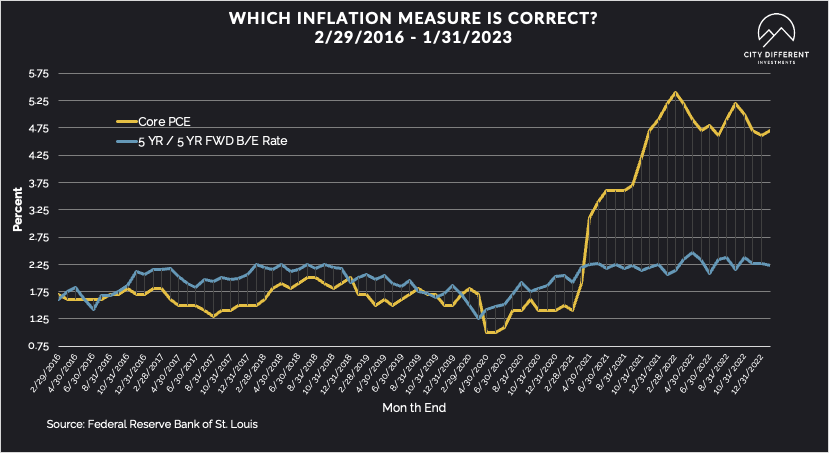

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate ended Friday at 2.29%, seven basis points higher than the February 17 closing of 2.22%. The 10-year Breakeven Inflation Rate ended the week at 2.38%, two basis points higher than last week’s observation of 2.36%. Given the stability of these measures, in light of new information, we question their value as an inflation forecasting tool.

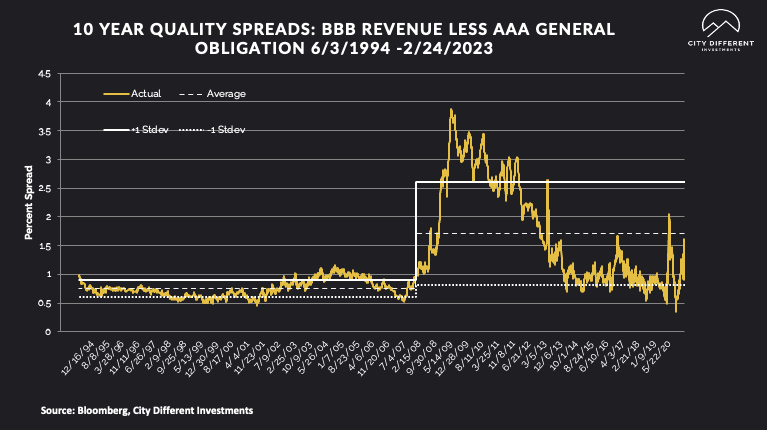

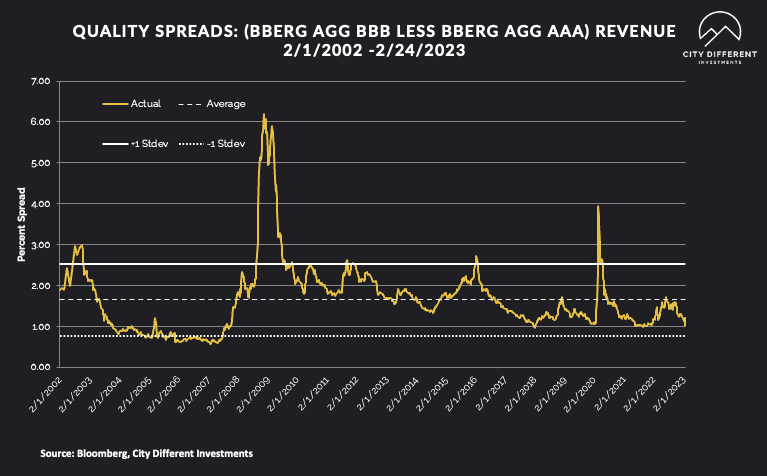

MUNICIPAL CREDIT

Municipal credit continued to narrow last week.

10-year quality spreads (AAA vs. BBB) were narrowed on the week from 1.22% to 1.15% (based on our calculations). The long-term average is 1.71%. By our thinking, lower-quality securities are still not attractive.

Quality spreads in the taxable market narrowed slightly, finishing at 1.02% vs. 1.20% last week.

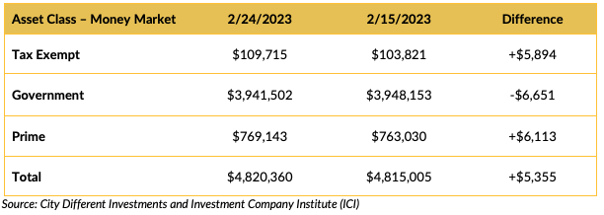

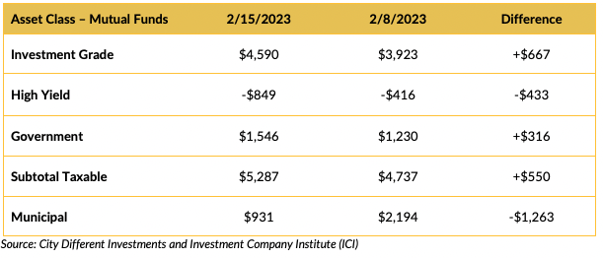

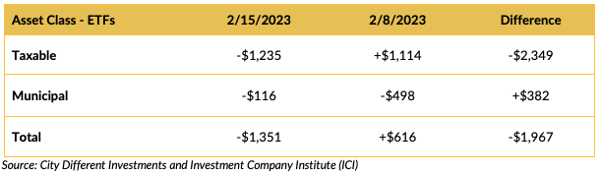

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

Prime money market funds won the week again!

Mutual Fund Flows (millions of dollars)

Municipal bond funds were the losers last week, shedding $1.3 billion on the week.

ETF Fund Flows (millions of dollars)

A quiet week for bond ETFs.

Other services that track mutual fund cash flows have reported negative flows for municipal bond mutual funds for the week ending February 15. This should be confirmed in next week’s ICI numbers.

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

We estimate that next week’s new-issue supply will be low, around $5.7 billion.

Total new issuance supply figures of $10 billion or more usually indicate weakness in new-issue supply pricing (higher yields).

CONCLUSION

The end of the pandemic era’s free money is certainly having once-in-a-lifetime impacts on some markets (particularly the Municipal bond market). Inflation is turning out to be harder to reign in than the market thought in January. We view higher yields as an opportunity for long-term investors, which means investors should be cautious putting money to work in the fixed-income markets. We believe dollar-cost averaging approach in this environment is warranted. Also, investing in areas where investors are getting paid to accept risk is prudent. Think of the shorter end of the fixed income markets.

And finally, for our smart friend, our commitment to a laddered structure is unchanged. The municipal yield curve has inverted, and a laddered structure hedges against that risk.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.