WEEK ENDING 2/10/2023

Highlights of the week:

- Chairman Powell stated disinflation “has begun” and added a big “but.”

- The Greek chorus of Fed officials that spoke in the week following Chairman Powell echoed his comments.

- Rates moved higher; maybe the market is starting to believe the Fed?

- The State of the Union address was the most combative and entertaining in memory.

A CITY DIFFERENT TAKE

This was another interesting week.

Chairman Powell spoke before The Economic Club of Washington, D.C. last week. In his comments, he said disinflation “has begun.” But Powell followed with, “If we continue to get, for example, strong labor market reports or higher inflation reports, it may well be the case that we have do (sic) more and raise rates more than is priced in.”

Chairman Powell’s comments seemed to take some steam out of the bond markets' beginning-of-the-year rally. We would say the fixed income markets are beginning to believe the Fed. This week's CPI report will be a major test. As the president reminded us in his State of the Union address on Tuesday, the big infrastructure spending programs and other legislative programs from this administration's first two years are just now being implemented — and their impacts on things (such as inflation) have not yet been seen. Read more of our reaction to the wild State of the Union address below in This Week in Washington.

The University of Michigan Consumer Sentiment Index showed that consumers think current conditions are better than the market expected (72.6 vs. 68.5), and one-year inflation expectations are slightly higher than forecasted (4.2% vs. 4.0%). All of which adds to the importance of this week’s CPI report for the markets.

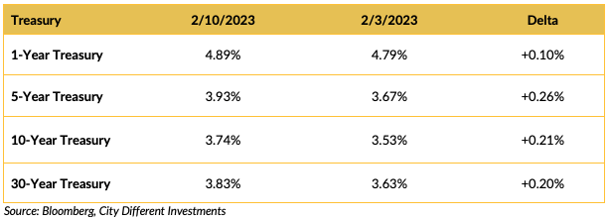

CHANGES IN RATES

Treasury rates moved higher on the week across the yield curve. The smallest increase was in the very short portion of the Treasury market. The slope of the one-to-10-year yield curve was at -1.15% vs. last week's -1.26%.

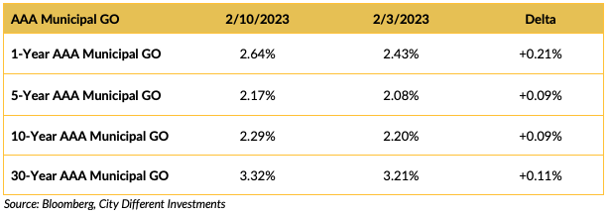

Rates in the municipal market also increased last week but at a much slower rate than in the Treasury market (shocking). The increase in new issue municipal supply this week may change things (read more to find out why). The one-to-10-year slope went more negative, finishing the week at -0.35 vs. The one-to-10-year slope went more negative, finishing the week at -0.35% vs. last week's -0.23%.

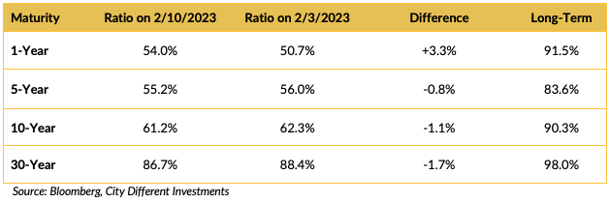

One-year ratios cheapened up, but all others were more expensive on a relative basis.

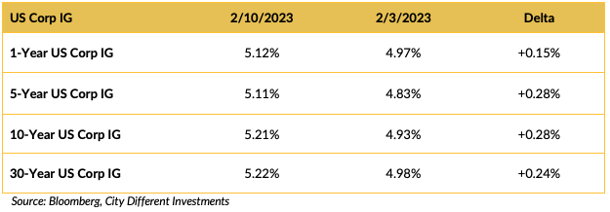

The week’s volatility was shared by the investment grade (IG) corporate market. 10-year IG corporates closed Friday at 5.21% vs. last week's 4.93%.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

We have mentioned in earlier weekly commentaries that this Congress will be “interesting,” and so far, it has not disappointed. Last week’s State of the Union address was the most combative and entertaining in our memory. President Biden put out a veritable buffet of government spending plans and set a social-spending trap, which some Republicans fell into.

In other news, the Los Angeles Times reported that the House subcommittee on “weaponization” of the Justice Department held its first hearing. We always thought smart lawyers avoided asking questions they didn’t know the answers to. Maybe these are not smart lawyers… or even lawyers?

Unfortunately for Republicans, the former Twitter executives they handpicked to serve as witnesses undermined their central thesis, testifying that they were not directed by the FBI or any other official to suppress information about Hunter Biden. The only revelation of federal interference with free speech concerned the previous administration’s efforts to get Twitter to censor Chrissy Teigen’s criticism of former President Trump.

Ready, fire, aim!

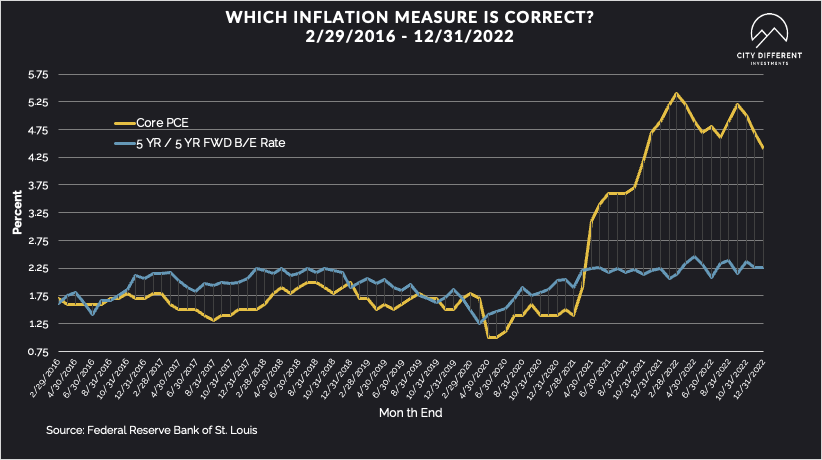

WHAT, ME WORRY ABOUT INFLATION?

The five-year Breakeven Inflation Rate ended Friday at 2.19%, two basis points higher than the January 27 closing of 2.17%. The 10-year Breakeven Inflation Rate ended the week at 2.33%, 11 basis points higher than last week’s observation of 2.22%. This is the first time we have observed such a divergence in these readings, and we guess that this week’s CPI report will indicate which observation is more correct.

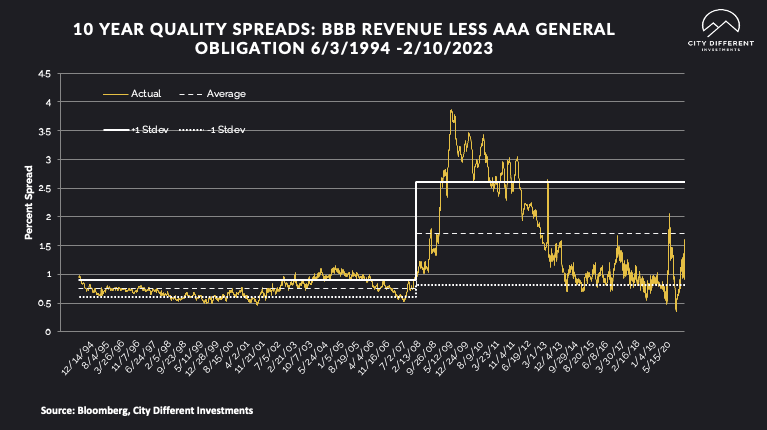

MUNICIPAL CREDIT

10-year quality spreads (AAA vs. BBB) were widened on the week from 0.91% to 1.32% (based on our calculations). The long-term average is 1.71%. By our way of the thinking, lower-quality securities are still not attractive but are moving in the right direction.

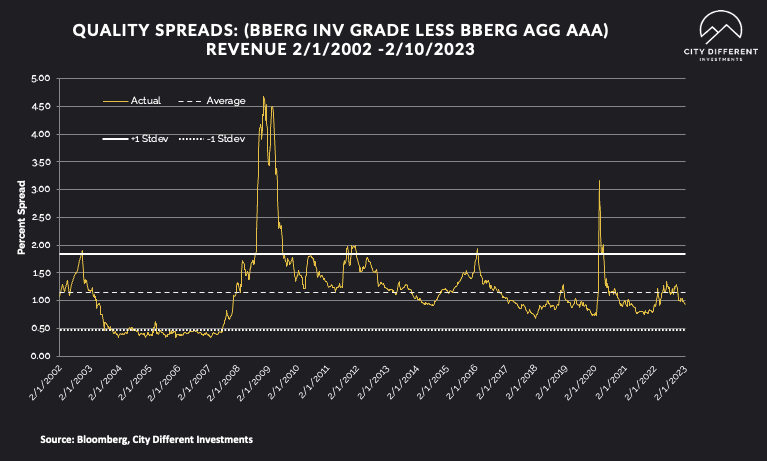

Quality spreads in the taxable market didn’t move much on the week, finishing at 1.18% vs. 1.14% last week. The taxable market didn’t have the same troubled press that the municipal market had.

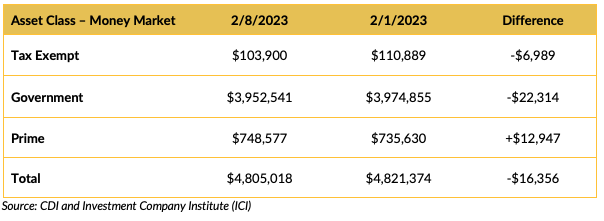

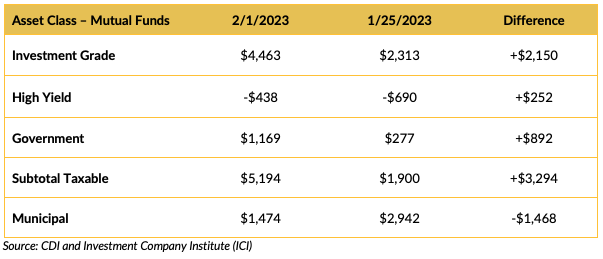

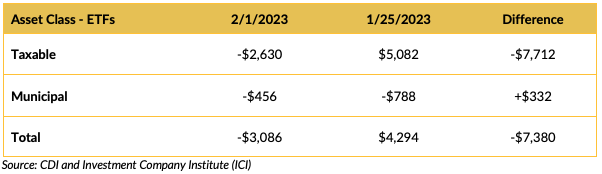

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

If you are not a Prime money market fund, it looks like investors don’t like you!

Mutual Fund Flows (millions of dollars)

Looks like IG bond funds won the last period. Municipal bond funds, not so much.

ETF Fund Flows (millions of dollars)

Finally, it wasn’t a good week for bond ETFs of any ilk!

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

We estimate that next week’s new issue supply will be low, around $7.4 billion. If this magnitude of new issuance supply persists, the end of the January effect could be upon us.

Total new issuance supply figures of $10 billion or more usually indicate weakness in new issue supply pricing (higher yields).

CONCLUSION

We feel this week’s volatility is indicative of what’s in store for the fixed income markets in 2023. So, buckle up!

We give a lot of credence to that old saw, “Don’t fight the Fed.”

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.