.png)

WEEK ENDING 11/18/2022

Happy Thanksgiving to all our readers.

We at City Different Investments (CDI) are very thankful for you and our clients, who continue to trust us with their assets. If you’re not a client yet, we look forward to proving that CDI is worthy of your trust.

Highlights of the week:

- Brainard and Bullard's comments seem to support the “Lower, Longer, and Higher” theory.

- The hangover from “free” money is manifesting itself in different ways. What’s next?

A CITY DIFFERENT TAKE

What a week this has been.

PPI seems to have confirmed CPI’s earlier indication of a possible slowing of inflation. Year-over-year core PPI came in at 6.7%, 0.05% below expectations, and September's year-over-year core reading was reduced by 0.01%. Investors need to keep in mind that one month does not a trend make, and the Fed is looking for a trend to confirm inflation is on the run.

Lael Brainard’s comments seem to support the “Lower, Longer, and Higher” theory for future Fed actions. (Lower rate increases in effect for a longer period and reaching a higher terminal rate.) A couple of cable talking heads took exception with St. Louis Federal Reserve President James Bullard's suggestion that the Fed Funds target rate could hit a high of 7%, given certain aggressive economic assumptions. The talking heads seem to be suffering from recency bias. Investopedia defines this condition as:

“A cognitive error identified in behavioral economics whereby people incorrectly believe that recent events will occur again soon. This tendency is irrational, as it obscures the true or objective probabilities of events occurring, leading people to make poor decisions.”

The hangover from Fed-engineered ultra-low interest rates is taking many forms. We view these events as nothing more than a reversion to the mean. As investors now have a competitive risk-free rate (Fed Funds target), many business models that needed near 0% interest rates to survive will begin to show cracks.

Couple this with the realization that more of the “tech whiz kids” are showing their clay feet. Elizabeth Holmes was sentenced to 11+ years in prison for fraud. Furthermore, CNN reported startling revelations of the FTX bankruptcy.

“A new court filing about Sam Bankman-Fried’s bankrupt companies reveals a crypto empire that was colossally mismanaged and potentially fraudulent — a ‘complete failure of corporate controls’ that eclipses even that of Enron.”

Sam Bankman-Fried has been called the "Crypto Madoff.”

And finally, Twitter is making headlines. CBS reported that a large number of Twitter employees resigned after receiving Elon Musk’s ultimatum to work longer hours or leave. Furthermore, employees that remained have been locked out of offices since Thursday. We thought that only happened in the MLB!

CHANGES IN RATES

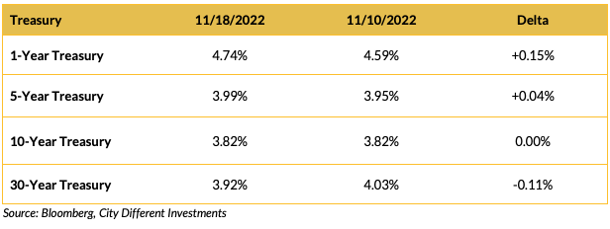

Treasury rates moved higher in the short end of the yield curve and lower in the long end. The inversion of the Treasury yield curve moved from -0.56% to -0.82%. Is that a precursor of a recession? That debate is on market participants' minds going into the Thanksgiving weekend. What does that mean for the December Fed meeting? As stated before, we believe the Fed’s course will be “Lower, Longer, and Higher.” That certainly sounds like Brainard’s and Bullard’s sentiments.

“That would be consistent with Fed Vice Chair Lael Brainard’s comment that a slower pace of increases seems appropriate. She also has suggested that further rate increases will be needed. Futures prices point to a peak fed-funds target of 5%-5.25% by next March, holding there until next November. Markets were roiled by a suggestion by St. Louis Fed President James Bullard that a policy rate as high as 7% might be needed to lick inflation, although that’s his worst-case scenario.”

A 50 basis point increase in the target rate seems to be locked in for the December meeting, but there is still a lot of data to be evaluated by a “data dependent” Federal Reserve.

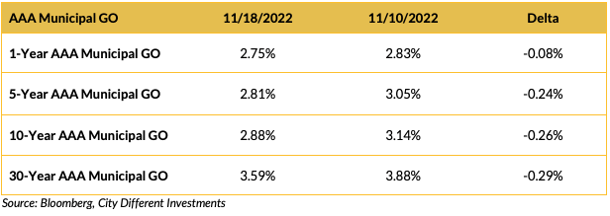

In contrast to the Treasury market, yields in the municipal market continued to move lower on the week across the yield curve. It looks like municipal market participants are positioning themselves for the January effect (a period when the municipal market outperforms due to low new issuance supply — one of the market's two most significant interest payments and maturity dates). This happens roughly 70% of the time but didn’t happen last year. The slope on the AAA general obligation municipal bond curve flattened last week, moving from a positive 1.08% to a positive 0.84%.

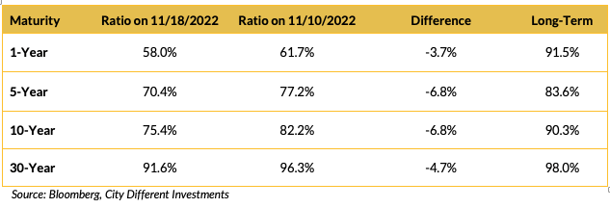

Muni/Treasury ratios richened on the week. We think market participants' enthusiasm for the potential of the January effect may be getting a little ahead of itself.

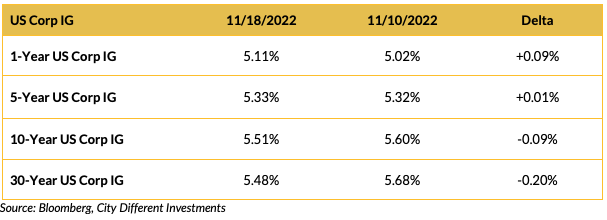

Investment-grade rates came lower on the week, especially at the long end of the yield curve.

THIS WEEK IN WASHINGTON

Well, the midterm counting is almost done. The much-anticipated red wave did not materialize. The Dems retained control of the Senate, releasing pressure on the Georgia runoff. It will be interesting to see how that concludes now that it's a choice between two candidates and not for control of the Senate.

The House turned over to Republican hands, and House Minority Leader Kevin McCarthy looks to be headed to the speakership. This has been a goal of his for a long time. However, McCarthy should be careful what he wishes for; with such a slim margin (currently estimated at 222 seats to 213), there will be 222 kings and queens, each with their own agenda. We saw what that was like in the Senate last year with the Dem’s slim majority. So far, it appears the initial Republican House agenda will be focused on the treatment of the January 6 insurrectionists and investigating the Biden family. We miss the days when our elected legislators actually legislated.

In a farewell address poorly attended by House Republicans and skipped entirely by McCarthy, outgoing House Speaker Nancy Pelosi said she would step down from a leadership role within the Democratic party. We believe in the sporting tradition that during the game, you try to knock the opponent's head off — but when the game ends, you shake hands, enjoy a beverage together, and maybe even share a couple of songs. Given the current state of partisan polarization, it seems as though the House does not share that tradition.

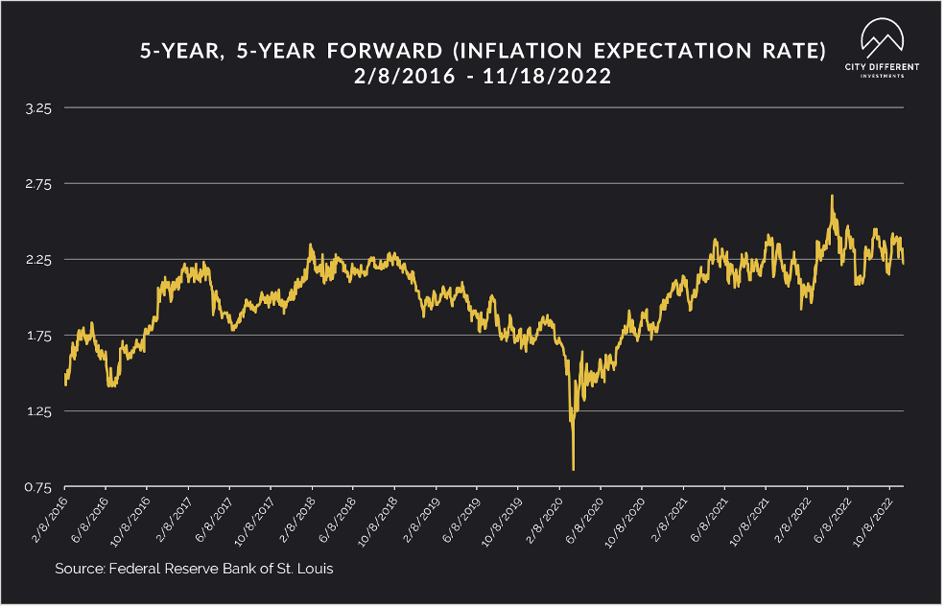

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate ended at 2.22%, nine basis points lower than the prior week closing at 2.31%. The 10-year Breakeven Inflation Rate ended the week at 2.25%, 14 basis points lower than the last reported observation of 2.39%. Both readings seem low, given where inflation is today.

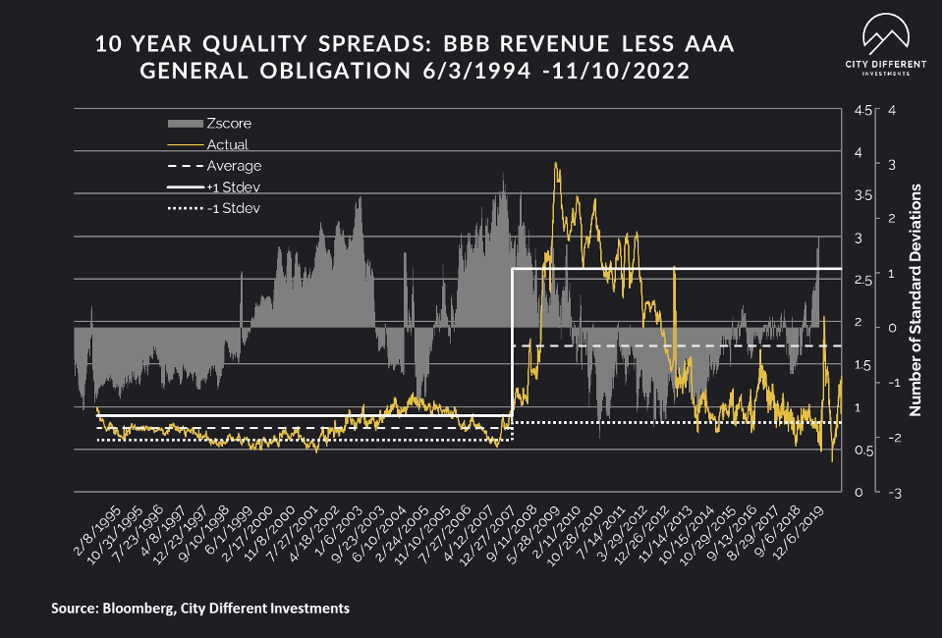

MUNICIPAL CREDIT

Long-term quality spreads continued to widen, moving further into the fair range, and are starting to pique our interest. Not quite soup yet, but more and more interesting each week. While we don’t think the move has been significant enough to change our strategic outlook toward credit, it's getting close.

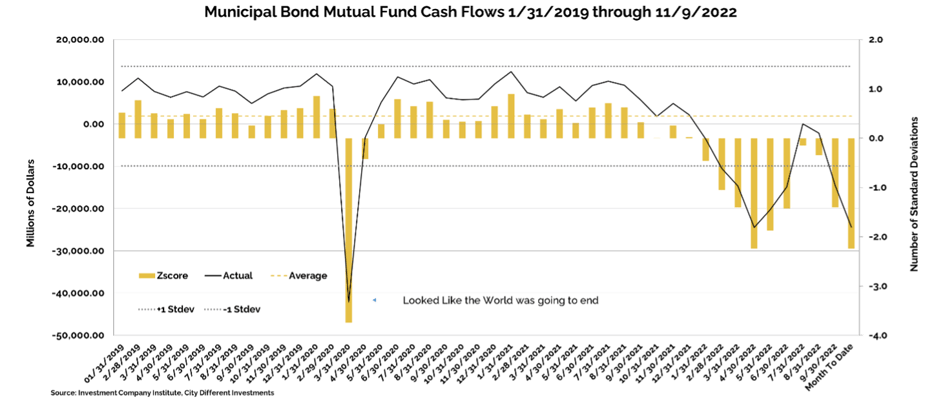

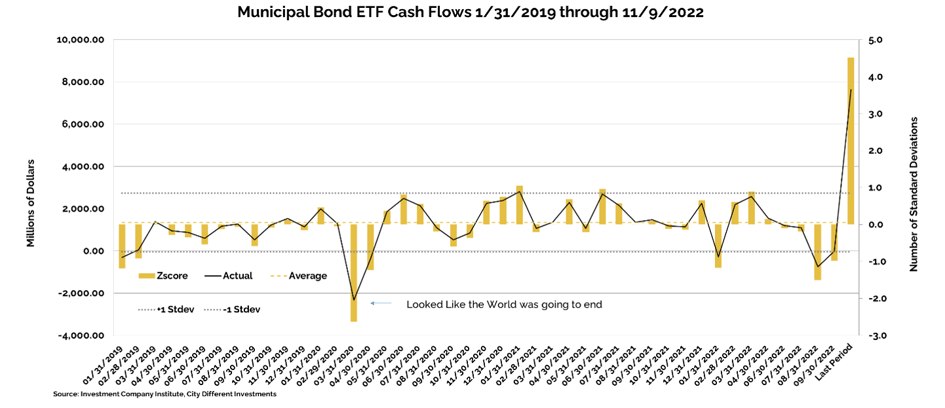

WHY IS THE MUNICIPAL MARKET BEHAVING THIS WAY?

Various sources are used to report cash flows related to municipal bond mutual funds and ETFs, all reporting at different times. The source we have chosen to use is the Investment Company Institute (I.C.I.). The I.C.I. reported weekly cash flows from municipal bond mutual funds for the week of November 9 as -$3.2 billion compared to -$3.8 billion from the week before.

Municipal bond ETF cash flows for the same period were +$942 million, compared to +$1.1 billion the prior week.

In its Municipal Markets Weekly newsletter, JP Morgan commented on cash flow data this week, stating that:

“Lipper reported combined weekly and monthly inflows of $605 million (2nd inflow in past three weeks) for the period ending November 16, decreasing YTD outflows to $112.4 billion. We believe that inflows will only be sustained if the recent two-week (44 bps) rally in 10-year UST rates continues, or at least UST yields remain near current levels.”

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

We expect new issue supply to be non-existent in the holiday-shortened week.

CORPORATE INVESTMENT GRADE AND HIGH YIELD OVERVIEW

In its weekly "Credit Flows" report, Wells Fargo commented:

“Most asset classes saw positive fund flows, as US IG and HY reported inflows of $0.3 billion and $3.6 billion, respectively, while Leveraged Loans had outflows of $0.6 billion. Internationally, Euro IG and HY had inflows of $0.7 billion and $0.2 billion, respectively, while EM credit had outflows of $0.3 billion. Supply was generally lower following last week’s surge, with US IG, HY, and Loans reaching $27.8 billion, $1.9 billion, and $7.3 billion, respectively. As of the prior week, dealers extended their net long in US IG to $7.3 billion, and reduced their net short in US HY to $0.5 billion.”

CONCLUSION

We have spent much time talking about the mean reversion impacts from years of Fed-induced free money: a competitive risk-free rate, faulty business models that need 0% rates to survive, and our old friend inflation. What can we learn from these events? None of this is new; the risks are just “dressed” differently. The scariest words in the investing business are, “this time, it's different.”

Here’s what we’ve learned over our careers, for which we’re very thankful:

- There are two ways to blow up an investment business: credit and leverage. These two factors are at the bottom of most business cycles and take a different shape each time. A successful investor learns to recognize these factors and take appropriate actions. Last time it was the financial crisis of the great recession and before the market, panic brought on by Long-term Capital Management.

- If you don’t understand it, don’t invest in it. No matter what the short-term returns are.

- Recency bias is real. An understanding and perspective of financial history will allow investors to avoid its pitfalls.

- It is really hard to analyze for fraud before the fact. How else did Sam Bankman-Fried attract so many big-name investors? As reported by Forbes:

“As the crypto exchange ballooned in size, it became a huge draw for venture capitalists eager to get in on the Bitcoin boom. In June 2021, FTX raised $1 billion at an $18 billion valuation from venture investors such as Paradigm, SoftBank, and Sequoia Capital. Three months later, FTX brought in a $421 million haul, pushing its valuation to $25 billion, from investors like Singapore-government owned investment firm Temasek, Tiger Global Management, and the Ontario Teachers’ Pension Plan. By January of this year, crypto prices were on the decline, but FTX charged ahead. Investors, many of whom had also pumped money into the earlier rounds, put another $400 million into FTX–at a $32 billion valuation.”

Due to the holiday, we will not publish our Week in Review next week — but look for our commentary the following week. Have a wonderful Thanksgiving.

.png?width=660&name=signature%20block%20(3).png)

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.