.png)

WEEK ENDING 12/02/2022

Highlights of the week:

- Latest jobs reports show a resilient labor market.

- Q4 earnings estimates are finally coming down.

- Introducing our new acronym, BARB: “Bonds are Back.”

A CITY DIFFERENT TAKE

The U.S. job market refuses to take a hint from the Federal Reserve as new job creation continues. Non-Farm Payroll was expected to increase by 200,000. The November numbers, however, showed an increase of 263,000, with an unemployment rate of 3.7%. The most surprising data was a jump in average hourly earnings, which increased by nearly 0.6%.

However, as the Fed goes into its blackout period, a 50-bps rate hike still seems to be locked in for December. Also, despite the strong jobs number, rate expectations have not changed since October’s inflation data. Remember, this was when PCE posted its smallest monthly increase since September 2021. The projected Federal Funds rate dropped on November 10 to 4.25% and has stayed there, according to Bloomberg interest rate probabilities. But an article in today’s Wall Street Journal indicates that because of the strong labor market, we could see a potential rate increase of 50 bps in February.

As a reminder, we at City Different do not think that inflation will come down swiftly. We continue to hold that the Federal Reserve will:

- Adjust rate hikes to go slower.

- Continue moving rates higher.

- Hold those rates higher for longer.

We do think that both the equity and fixed income markets have gotten ahead of themselves, and we could see the landing zone for the Federal Funds rate be somewhere between 4.25% and 5.25%.

In other news, welcome to a new CDI acronym: BARB. “Bonds are Back.”

As we enter into a new investing regime with higher rates and inflation, bond yields certainly look attractive. To quote Bloomberg, yields among corporate bonds have not been this high in nearly 12 years. How far we have come in yields can be demonstrated by the difference in YoY yield for Moody’s Seasoned Aaa Corporate Bonds, which moved from 2.61% at the start of November 2021 to 5.09% on November 1, 2022. There is no denying that 2022 has been a tough year for bonds. Similarly, rate changes on the municipal side make bonds attractive. The 2-year and 5-year parts of the Municipal Market Data (MMD) moved ~227 bps and ~196 bps on the upside, respectively.

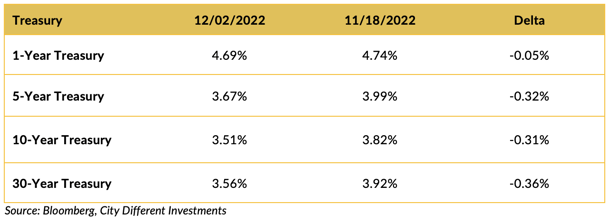

CHANGES IN RATES

A lot has happened in the last two weeks. Treasury yields have moved significantly lower, and the inversion of the yield curve, as measured by the yield differentials between one and 30 years, has increased from -0.82% to -1.13%. This is a big deal and indicates that market participants believe a recession will likely happen soon. This should lead the Fed to pause or reverse its inflation fight.

We do not share this view and believe that Powell’s speech last week did nothing to alter the “slower, higher, longer” mantra. Friday’s jobs report and the earlier JOLTS report (of more than 10 million job openings) do not appear to support an economy on the brink of recession.

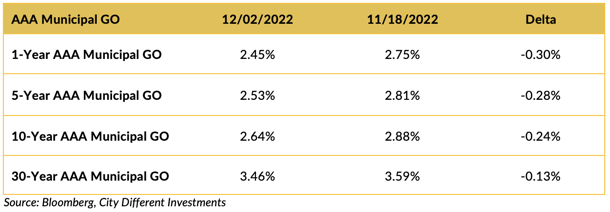

Yields in the municipal market continued to move lower across the yield curve, moving in line with the Treasury market (for a change). By contrast, the municipal bond yield curve is positively sloped from one to 30 years. That positive slope increased over the last two weeks, moving from +0.84% (on November 18) to +1.01% (on December 2). It seems like municipal market participants are anticipating a positive January effect.

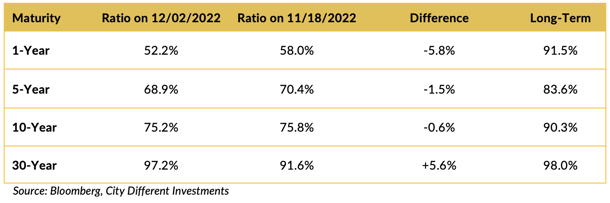

Muni/Treasury ratios richened on the week, except in the long end of the market. Market participants' showing enthusiasm for the potential of the January effect may be getting ahead of themselves.

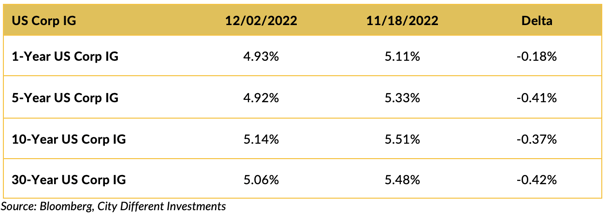

Investment-grade rates followed Treasury rates lower over the two-week period.

THIS WEEK IN WASHINGTON

As party control changes in the House, the White House is bracing for a possible Republican investigation into the Biden administration. The outcome could impact the President’s standing for the 2024 election. Otherwise, it’s business as usual for Congress.

WHAT, ME WORRY ABOUT INFLATION?

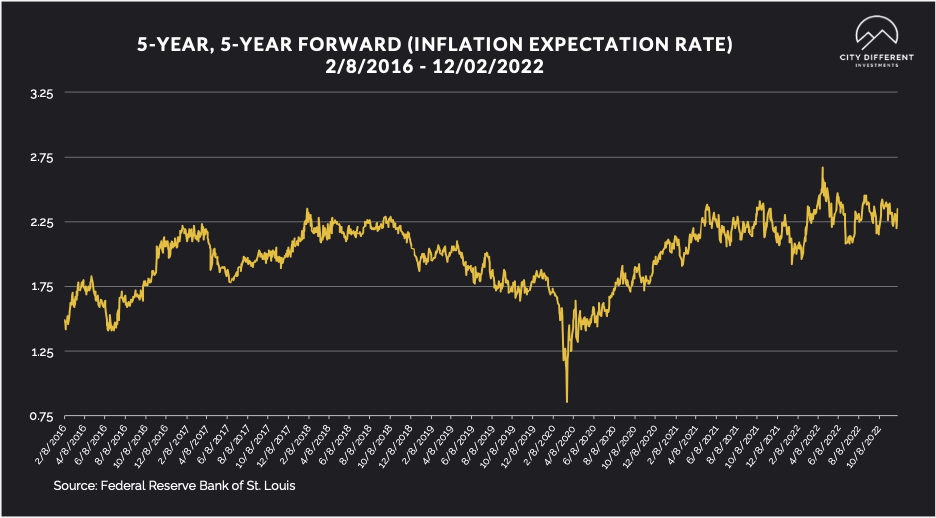

The 5-year Breakeven Inflation Rate ended Friday at 2.35%, 13 basis points higher than November 18, closing at 2.22%. The 10-year Breakeven Inflation Rate ended the week at 2.43%, 18 basis points higher than the November 18 observation of 2.25%. Both readings seem low, given where inflation is today.

MUNICIPAL CREDIT

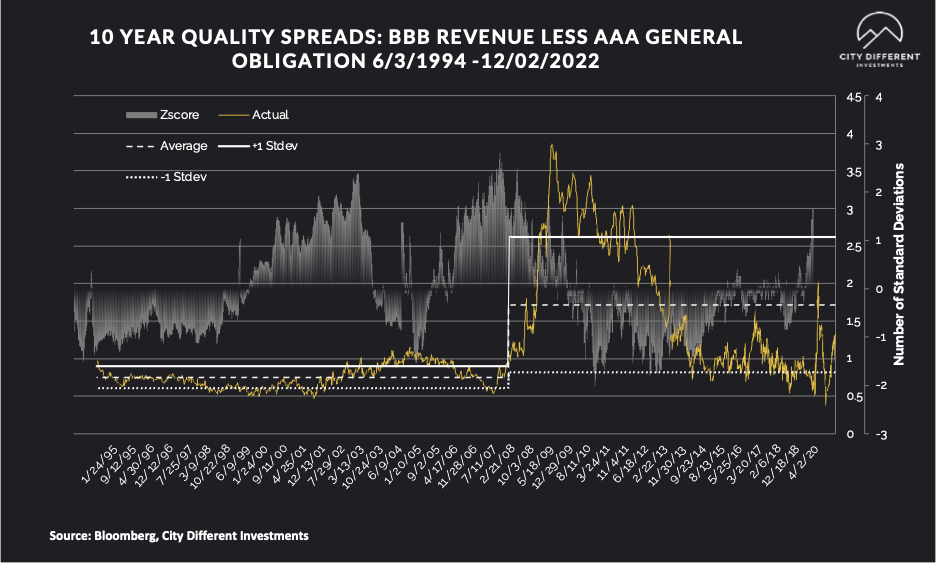

10-year quality spreads (AAA vs. BBB), as measured on December 2, were 1.30%, still below the long-term average of 1.72%. This reading is at the lower end of the fair territory (as we define it). We still do not think that investors are “getting paid” to take credit risk with forecasts of a recession (even though we believe the likelihood of a significant recession is low). We would need quality spreads to move into the upper portion of the fair territory before beginning a strategic position.

WHY IS THE MUNICIPAL MARKET BEHAVING THIS WAY?

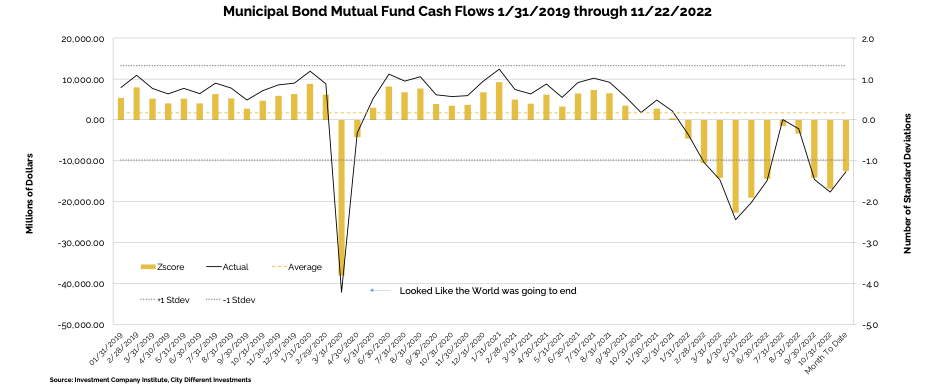

Various sources are used to report cash flows related to municipal bond mutual funds and ETFs, all reporting at different times. The source we have chosen to use is the Investment Company Institute (I.C.I.). The I.C.I. reported weekly cash flows from municipal bond mutual funds for the week of November 16 and 22 combined was -$2.8 billion compared to -$3.2 billion from the week of November 9.

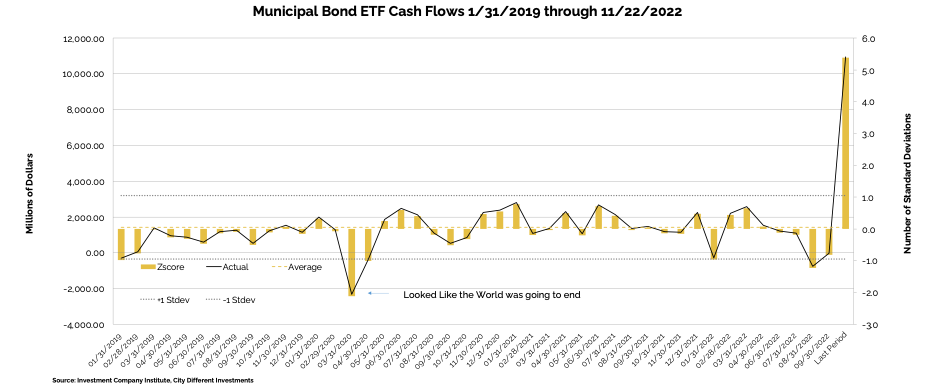

Municipal bond ETF cash flows for the same combined period were +$3.3 billion, compared to +$942 million the week of November 9.

Other cash flow sources:

In its Municipal Markets Weekly newsletter, JP Morgan commented on cash flow data this week, stating that:

“Lipper reported combined weekly and monthly inflows of $916 million for the period ending November 30, decreasing YTD outflows to $111.9 billion. The inflows were driven by monthly reported ETF funds, while open-end mutual funds still posted $1.9 billion combined weekly and monthly outflows. High Yield funds recorded $590 million of outflows, Intermediate funds saw $272 million of outflows, while Long Term funds saw $1.1 billion of inflows. Municipal ETFs registered $2.8 billion of inflows.”

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

We expect new issue supply to slowly recover from the Thanksgiving holiday before shutting down for the Christmas holiday.

CORPORATE INVESTMENT GRADE AND HIGH YIELD OVERVIEW

In its weekly "Credit Flows" report, Wells Fargo commented:

“The Fed’s communication challenge. On Wednesday, in a much-anticipated speech before the Brookings Institution Fed Chair Powell failed to push back on the recent significant loosening of financial conditions that has stocks now 8% higher and 10-year Treasury yields 57bps lower than after the November 2 FOMC meeting where Powell delivered a solidly hawkish message. Such loosening of financial conditions is entirely contrary to his message that monetary policy needs to be in the restrictive territory. That alone is reason to be defensive ahead of CPI/FOMC/ECB the week after next.

In addition to that today’s jobs report for November highlights the Fed’s formidable communication challenge as average hourly earnings are now increasing for the first time since March. Recall that wages are the main driver of CPI and PCE and thus really there are few signs the Fed is making any progress in its quest to combat inflation. Furthermore — and Fed Chair Powell pointed this out — Inflation data recently has had this tendency to come in soft (like in October) only to come back stronger the following month. We are looking for Fed Chair Powell to come off surprisingly hawkish at the next FOMC meeting and so would be short into the week after next.”

CONCLUSION

A robust and relentless job market makes a case for a Fed rate hike, possibly leaning into February and resulting in a higher terminal rate.

We think both credit and equity markets have gotten ahead of themselves, and we are still in the midst of a slower, higher, and longer rate hike cycle.

And with higher yields, the new acronym for the bond market is BARB: “Bonds are Back.”

.png?width=660&name=signature%20block%20(3).png)

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.