.png)

WEEK ENDING 11/04/2022

Highlights of the week:

- The Fed: Slower, Longer, Higher.

- Whether you look at the JOLTS numbers or Friday’s payroll numbers, the jobs market looks strong. No reason for the Fed to relent.

- We are getting more excited about investing in bonds, but not all bonds. There are still some risk factors, such as a flat yield curve and negative real yields for longer maturity securities.

A CITY DIFFERENT TAKE

Well, Chairman Powell’s news conference was one for the record books. The stock and bond markets both rallied after the release of the Fed’s November policy announcement. Initially viewed as a less hawkish approach toward future rate increases, the chairman took the stage and dashed both markets’ hopes for a pause. Even a redefined pause. The long and short of it is, expect:

- A potentially slower pace of rate increase.

- A potentially longer period of restrictive policy rates.

- A potentially higher than expected terminal policy rate.

All data dependent, of course.

In our estimation, this is a great environment to begin dollar-cost averaging into the bond market, but not all bond market segments. For example, we like short-maturity bonds out to 5 years. The flat and negative yield curves make longer maturity bonds less inviting. Given current yield spreads, investors, in our opinion, should focus on higher quality vs. lower quality securities.

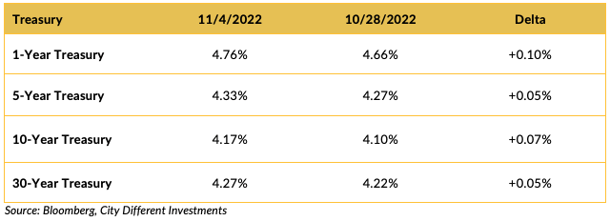

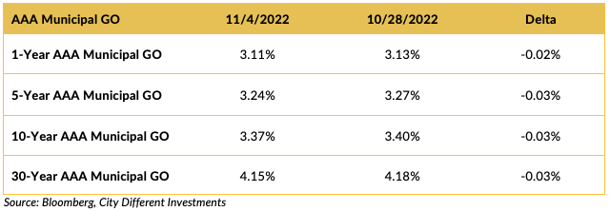

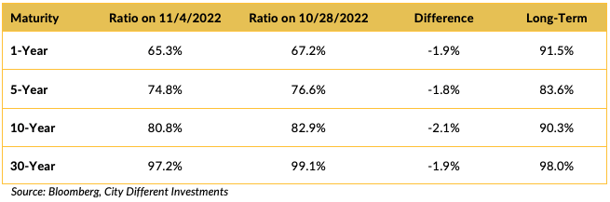

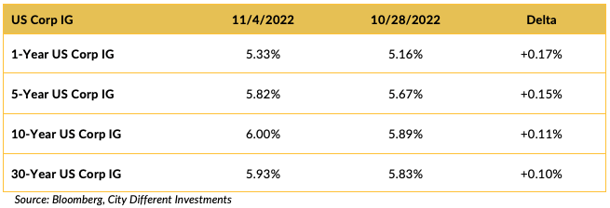

CHANGES IN RATES

Treasury rates moved higher on the week. Chairman Powell’s news conference after the Fed’s initial announcement of a change in the target short-term rate certainly added volatility to both the stock and bond markets.

The municipal market yields moved lower on the week. The market either did not believe Chairman Powell or was reacting to one of the lowest new issuance weeks of the year. We think it was the latter.

Muni ratios moved lower on the week, a product of the above observations.

Investment-grade rates came higher on the week.

THIS WEEK IN WASHINGTON

It’s only days away from the midterm elections and the silly season of campaign commercials is reaching a crescendo. We want to throw our shoes at these ads; here’s hoping your televisions survive. After watching the Sunday morning news shows, it seems like most races are too close to call and all political party operatives are declaring victory. Given the 40+ million early votes that have been cast, the final decision may not be known for some time.

There is one troubling trend we have noticed, and it affects both parties. It seems that some of our representatives in Washington are growing more isolationist in their rhetoric. U.S. support for Ukraine is beginning to be questioned. CNN posted the following story, “Liberal Democrats call on Biden to shift Ukraine strategy.”

“More than two dozen liberal House members are calling on President Joe Biden to shift course in his Ukraine strategy and pursue direct diplomacy with Russia to bring the months-long conflict to an end.”

Republicans are sending the same message.

“Rep. Marjorie Taylor Greene vowed Thursday that ‘not another penny’ of U.S. funding would be spent to help Ukraine defend itself against Russia if Republicans take control of Congress after the midterm elections.”

Kevin McCarthty clarified prior statements, so it may funding continues under a Republican majority, but with more thought and accountability.

“After House Minority Leader Kevin McCarthy suggested last week that Republicans might pull back funding for Ukraine next year if they take the majority, the GOP leader has worked behind the scenes to reassure national security leaders in his conference that he wasn’t planning to abandon Ukraine aid and was just calling for greater oversight of any federal dollars, sources told CNN.”

Both parties sound like they are hoping to win the Nevil Chamberlin award.

We’ve shared this Mark Twain quote before: “History never repeats itself, but it does often rhyme.”

The rhyme we’re thinking of is the Spanish Civil War of 1936. The United States took a strong isolationist stance wanting to stay out of Europe’s problems. But mollifying a dictator like Hitler eventually led to World War II. What has lending economic and other support to Ukraine done so far?

- Highlighted that Russia’s military is a paper tiger.

- Improved and expanded the NATO alliance.

- Given China second thoughts, perhaps, when it comes to Taiwan.

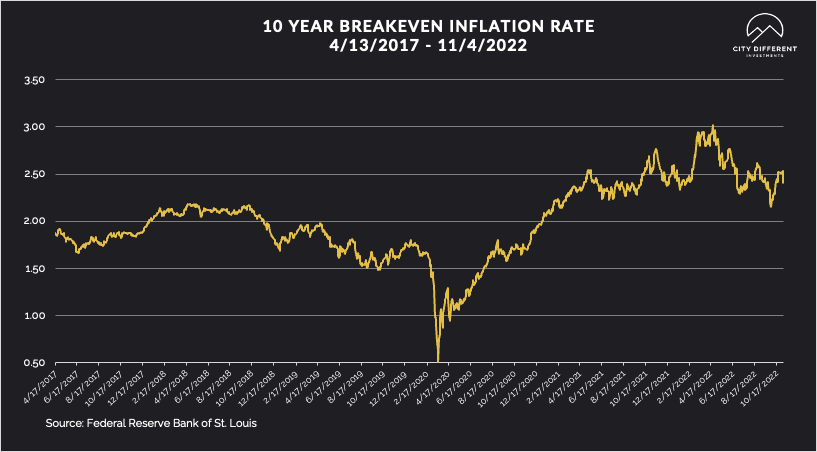

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate ended at 2.35%, 5 basis points lower than the prior week closing at 2.40%. The 10-year Breakeven Inflation Rate ended the week period at 2.48%, 3 basis points lower than the last reported observation of 2.51%. Both of these readings seem low, given where inflation is today.

Here are some interesting facts about the current levels of inflation:

- Inflation is a worldwide problem and U.S. inflation rates are amongst the lowest in the world. The analogy of being the best dirty shirt in a pile of dirty clothes seems appropriate.

- If you believe, as we do, that Milton Friedman was correct, and inflation is a monetary phenomenon, then M2 money supply is beginning to slow-

-M2 growth from 1/1/2020 through 12/1/2020 was 24.2%.

-M2 growth from 1/1/2021 through 9/1/2022 was 11.0%.

We know that the administration in power gets blamed for everything that is happening. But the impacts of their policies usually have a lag effect (around 12 to 18 months, from what we remember from our undergraduate political science classes). We will leave you all to draw your own conclusions.

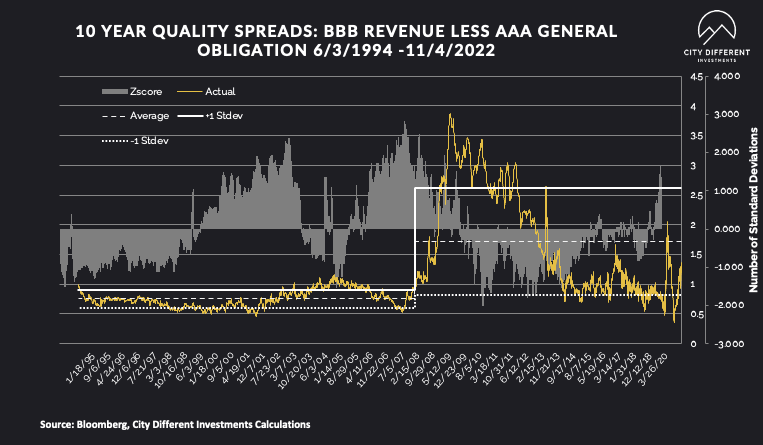

MUNICIPAL CREDIT

Long-term quality spreads continued to widen, moving further into the fair range, starting to pique our interest. Not quite “soup” yet, but more and more interesting each week. While we don’t think the move has been significant enough to change our strategic outlook towards credit, it's getting close.

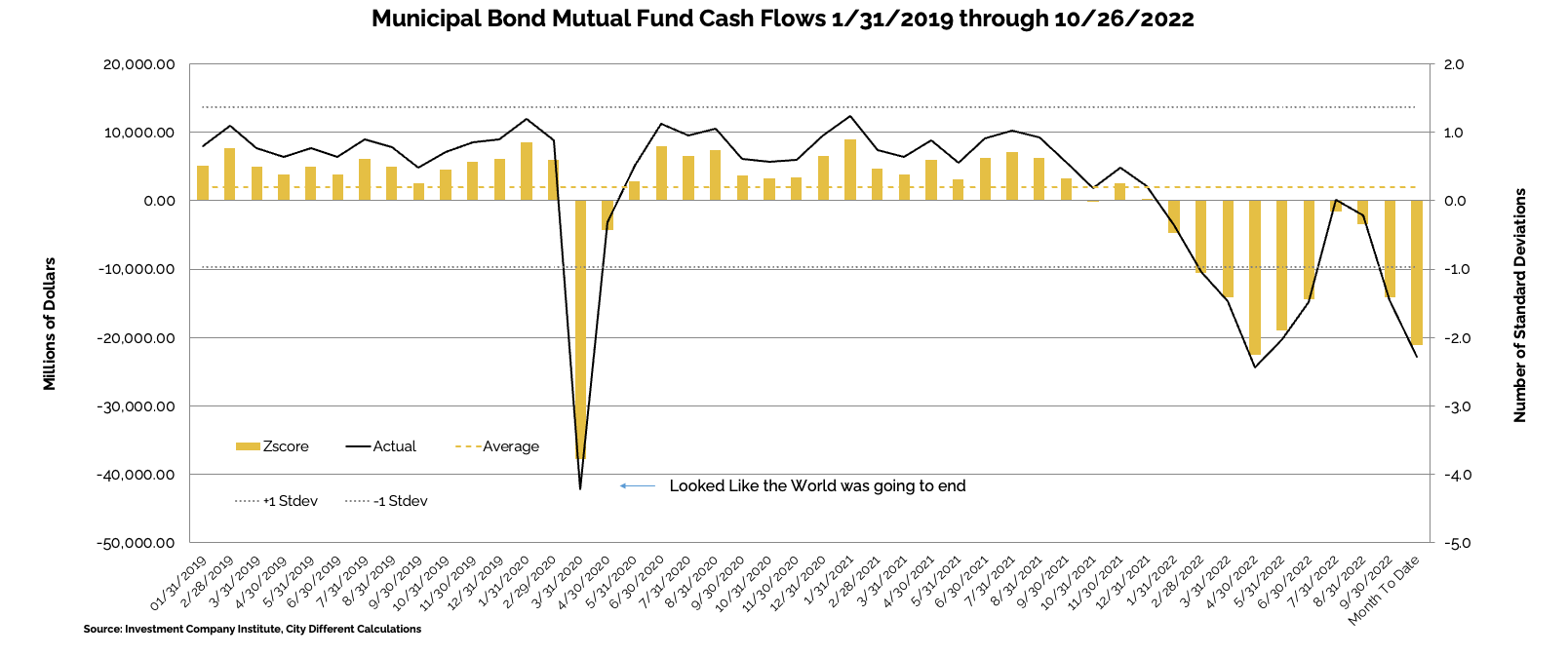

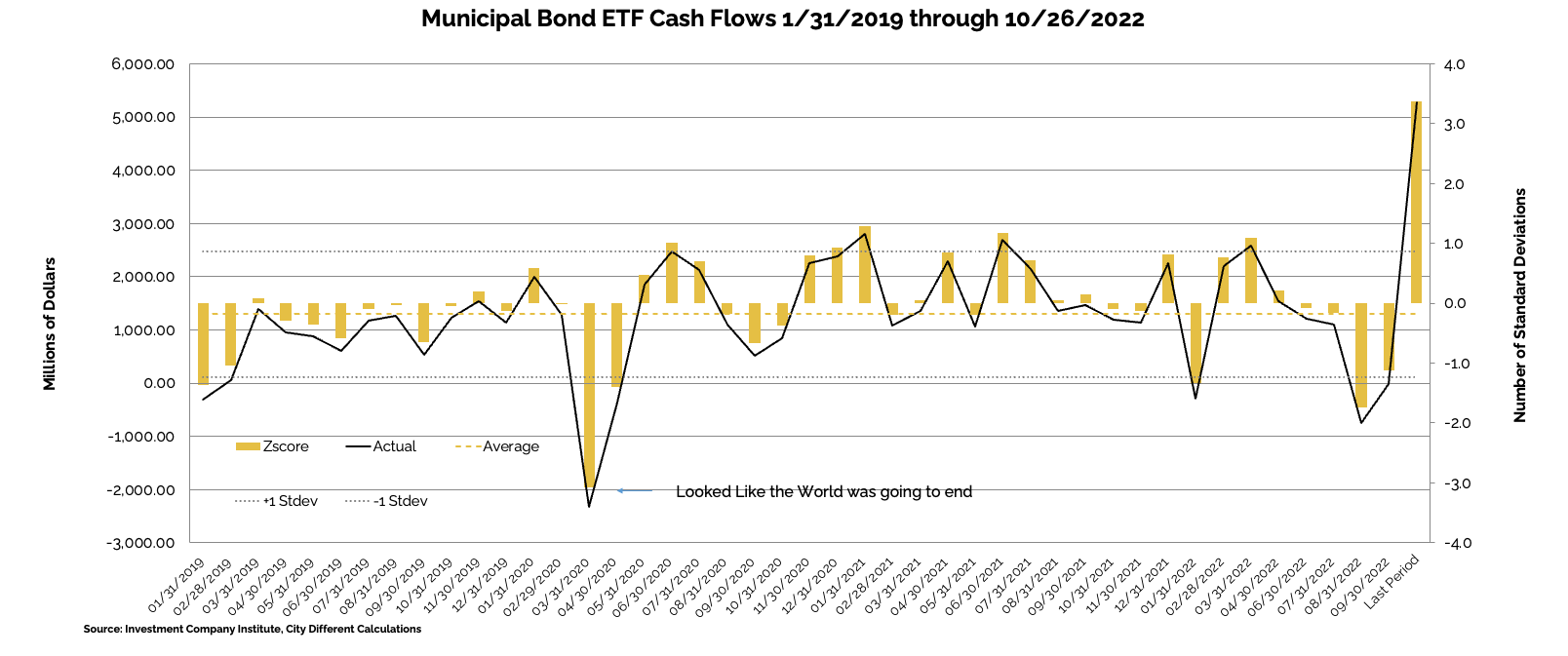

WHY IS THE MUNICIPAL MARKET BEHAVING THIS WAY?

Various sources are used to report cash flows related to municipal bond mutual funds and ETFs, all reporting at different times. The source we have chosen to use is the Investment Company Institute (I.C.I.). The I.C.I. reported weekly cash flows from municipal bond mutual funds for the week of October 26, as -$3.8 billion compared to -$3.9 billion from the week before.

Municipal bond ETF cash flows for the same period were +1 billion, compared to +334 million the prior week.

Other cash flow sources:

Lipper reported combined net weekly and monthly inflows of $926 million, marking the third inflow in the past 43 weeks. For the period ending November 2, muni ETFs saw combined weekly/monthly inflows of $4 billion (94% into just two ETFs), versus open-end outflows of $3.1 billion. YTD outflows total $103.9 billion.

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

In its Municipal Markets Weekly newsletter, JP Morgan commented on the supply picture this week, stating that:

“Next week, we expect total supply of $5.5 billion, or 61% of the 5-year equivalent week average ($9 billion). We anticipate tax-exempt supply of just $3.6 billion (47% of average), and taxable/corp cusip supply of $1.9 billion (140% of the average).”

The supply picture does not get interesting until it exceeds $10 billion tax-exempt issuances in a given week.

CORPORATE INVESTMENT GRADE AND HIGH YIELD OVERVIEW

In U.S. Investment Grade land, IG Credit primary market supply picked up last week with $31.5 billion in issuance.

In its weekly "Credit Flows" report, Wells Fargo commented:

“An Arm and a Leg. With a tight labor market and a very hawkish Fed all focus next week on US CPI for October to be released Thursday. Recall that September’s +6.6% YoY reading was a new cycle high and in fact the most in 40 years. Over the past twelve months core CPI came in higher than consensus eight times, matched twice and twice came in below two times. On average numbers exceeded consensus by 0.1% monthly. That suggests economists have not yet found the recipe to model inflation in this highly unusual environment, and that the relevant risk we should prepare for is another surprise to the upside — which would certainly be negative for risk assets. Our economists are in line with consensus at +6.5%.

Tight labor market. While the jobs report for October showed continued strong hiring with nonfarm payrolls at +233k (vs. +200k consensus) and upward revisions the more important underlying details were mixed-to-negative. For example the increase in the unemployment rate to 3.7% (from 3.5%) is encouraging as it shows progress in the Fed’s fight against high wage inflation. However this resulted in part from a 0.1% decrease in the labor participation rate, which runs counter to what the Fed is trying to do. In terms of wages Average Hourly Earnings surprised to the upside at +0.4% MoM (vs. +0.3%), but YoY number matched expectations for a decline to +4.7% from +5.0%. Worrisome as it shows a stronger pace of current wage growth.

Powell’s Volcker moment, redux, redux. Powell’s Volcker moment was his speech at Jackson Hole in August (Powell's Volcker Moment). Powell’s Volcker moment, redux, was when he followed through on that hawkish message at the September FOMC meeting (Powell’s Volcker Moment, Redux). Wednesday’s FOMC developments were pretty much as hawkish as it gets. In fact, instead of the discussion about lowering the pace of future rate hikes (after Wednesday’s 75bps as expected) making the FOMC come off as dovish, the impact was merely to prevent a much more significant sell-off in risk assets and increase in rates. Still equities ended down 2.5%, rates up 6bps and a reversal in credit spreads from tighter to wider.”

CONCLUSION

Chairman Powell’s news presser was certainly a thing to behold. Passages like the following roiled both the stock and bond markets:

- In the WSJ, he explained that even if rate increases slow, “we may ultimately move to higher levels than we thought at the September meeting.”

- In the same article, he added, “the question of when to moderate the pace of increases is now much less important than the question of how high to raise rates and how long to keep monetary policy restrictive.”

- The WSJ also reported on Powell stating “It is very premature to be thinking about pausing,” he said. “We think we have a ways to go.”

And the jobs report did nothing to make the market think there was any relief to higher rates in sight. Sometimes a long-term investor and a quarterback need the same kind of outlook on the world. As the fictional Ted Lasso put it, “You know who the happiest animal in the world is? A goldfish. Why? It's got a 10-second memory.”

Yes, 2022 has been terrible in terms of returns for both stock and bond markets. But that is the past and you cannot drive a car by only using the rear-view mirror. Our equity colleagues tell us stocks are on sale. Yield levels are finally making sense in the bond markets. At the end of last year, the 10-year Bloomberg municipal benchmark was yielding less than 1%. Today it is yielding more than 3%, an increase of nearly 3 percentage points. (We rounded, so bear with us). What the means is that last year the income cushion of that index was almost nonexistent. Today, not so much.

September’s Core PCE reading was 5.1%, the Fed’s target is 2%. That may be a stretch objective, but let’s say the Fed reduces core PCE to 3.5%. That means the 5-year AAA general obligation bond’s real yield is -0.26% (subtracting 3.5% from 3.24% equals -0.26%). That number is within our definition of fair. By our calculations, the real-yield fair range for a 5-year AAA general obligation bond is +2.29% to -0.77% over/under core PCE.

In our experience, it is a fool’s errand to try to pick a bottom or top of a market. We believe that when the fundamentals turn it is usually in the long-term investor’s best interests to forget recency bias and look forward.

.png?width=660&name=signature%20block%20(3).png)

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.