.png)

WEEK ENDING 10/6/2023

- McCarthy ousted as inmates take over the asylum.

- Fixed-income yields continue to move higher; investors leave bond funds for the safety of money market funds.

- Is this the moment for prudent risk-taking? We think so.

A CITY DIFFERENT TAKE

What a week! In what has been described as a Republican civil war, the Speaker of the House was ousted for the first time in our history by a no-confidence vote essentially. The temporary deal that prevented a government shutdown runs out in about 40 days, and the House is in chaos. Not only is the government's ability to operate in question, but so is U.S. funding for the war in Ukraine. As we have mentioned before, funds for Ukraine have far-reaching ramifications, including:

- How the U.S. is viewed by its allies.

- The role of NATO in the world.

- European border stability.

- The potential risk of a Taiwanese confrontation with China.

Domestically, Friday’s jobs report surprised market participants. Expectations were for an increase in nonfarm payrolls of 170,000 and continued negative revisions to the prior month's numbers. Neither happened. September saw an increase of 336,000 nonfarm payrolls, while the previous couple of months were revised upwards. The only thing keeping market participants from jumping off a proverbial cliff was the monthly hourly earnings came in at 0.2%, below estimates of 0.3%. Jumps are growing, and wage inflation is reasonable. We guess that the UAW and Kaiser Permanente strikers are relieved to hear this. Although, to be fair, the UAW did reduce its wage increase demand from 40% to 30%, and there seems to be some positive movement in the negotiations.

Next week, we may see who the new Speaker of the House is and get a couple more inflation reports.

Oh yes, before we forget, Happy Columbus Day/Indigenous Peoples Day. A shortened work week will impact new issue municipal bond supply.

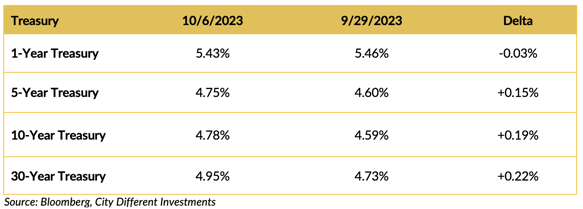

CHANGES IN RATES

Treasury yield moved higher on the week. The yield curve, while still inverted, steepened. The spread between the two-year and 10-year Treasury securities was -0.30%, another big move. Last week, the two-10 spread was -0.47%. The payroll numbers were a big surprise, offset by moderate wage data.

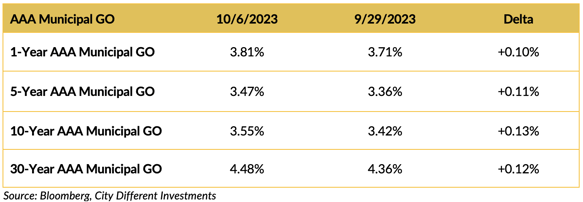

The municipal bond market yields moved higher on the week as well. Many new issue deals were delayed, given the interest rate volatility. Next week's supply looks to be about $4.5 billion.

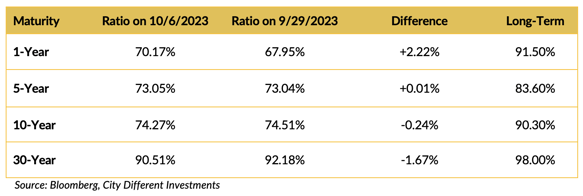

The municipal/Treasury ratios were mixed across the board, as the municipal market adjusts to the unique challenges facing it.

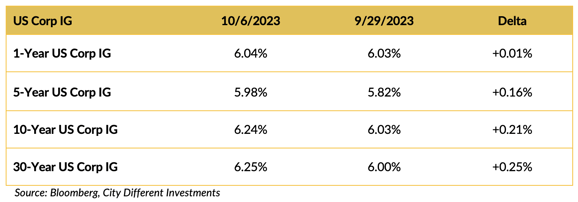

Corporate yields moved higher last week.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

This was a historic week in D.C. Never before has a Speaker of the House been ousted on what amounts to a no-confidence vote. Liz Cheney praised the Democrats on a “principled” vote.

“She said Democrats made a ‘principled’ decision in choosing not to save McCarthy’s job given his track record, citing McCarthy’s decision to continue abiding and apologizing for Trump. All present 208 Democrats, along with eight Republicans, voted for McCarthy to be removed.” Liz Cheney

We are not so sure that her opinion may have been tinged with a little personal bitterness. Sometimes, the devil you know is better than the devil you don’t know. Especially looking at the slate of contending Speaker replacements. The Republicans certainly had a sense of urgency. After the vote, the House took the week off. The election process for Speaker starts this week, and we wonder how many ballots it will take this time. The only things in the balance are a government shutdown in about 40 days and funding for Ukraine.

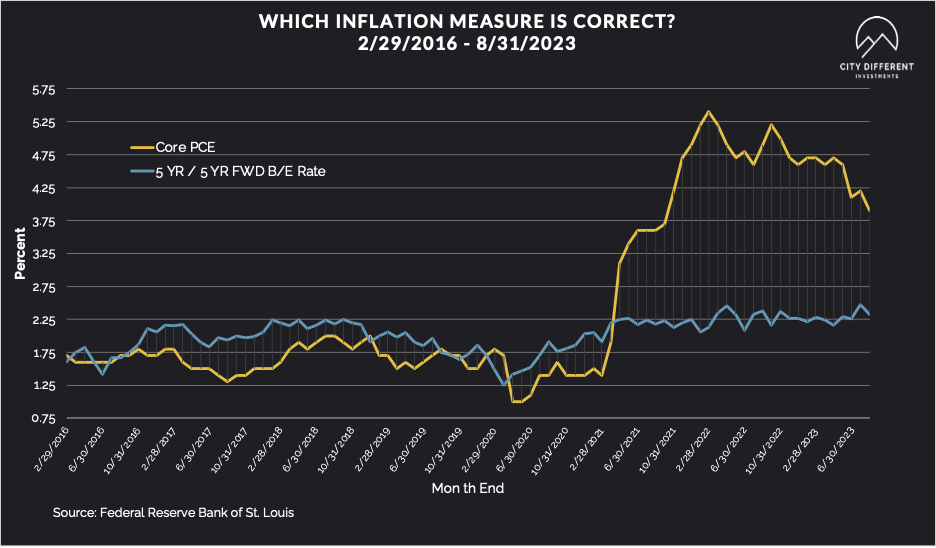

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate finished the week at 2.45%, three basis points lower versus the September 29 close of 2.48%. The 10-year Breakeven Inflation Rate finished the week at 2.31%, four basis points lower than the September 29 close.

Here is something new. Based on Friday’s close, the 10-Year Treasury yielded 4.80%, and August’s Core PCE reading was 3.90%. That equates to a real yield of +0.90%, or -0.56 standard deviations below the long-term average. That would put it on the rich side of the fair territory as we calculate it.

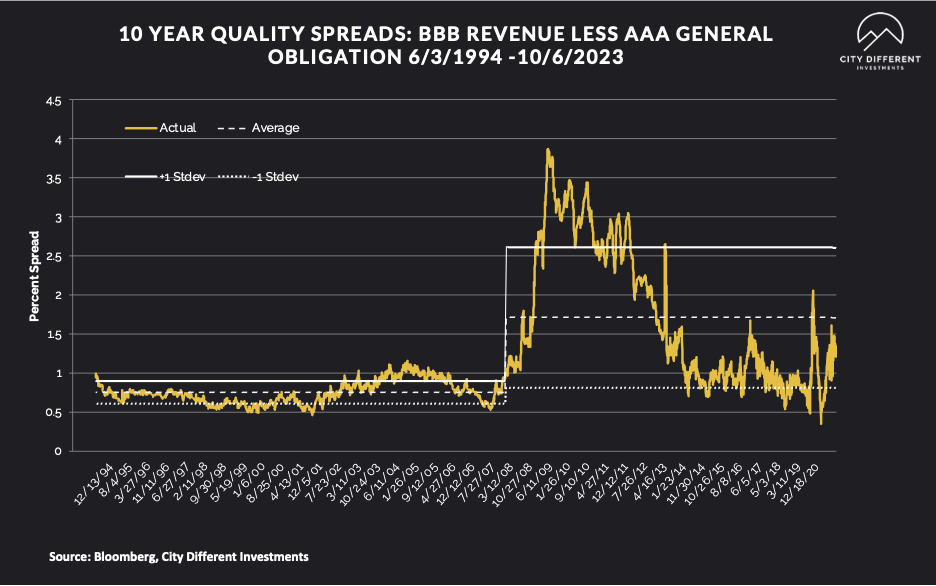

MUNICIPAL CREDIT

10-year quality spreads (AAA vs. BBB) as of October 6 was 1.33%, four basis points higher from the September 30 reading of 1.29% (based on our calculations). The long-term average is 1.71%. By our way of thinking, we still think lower-quality securities are not attractive. Municipal market credit spreads usually take a little more to adjust, given a significant baseline market revaluation.

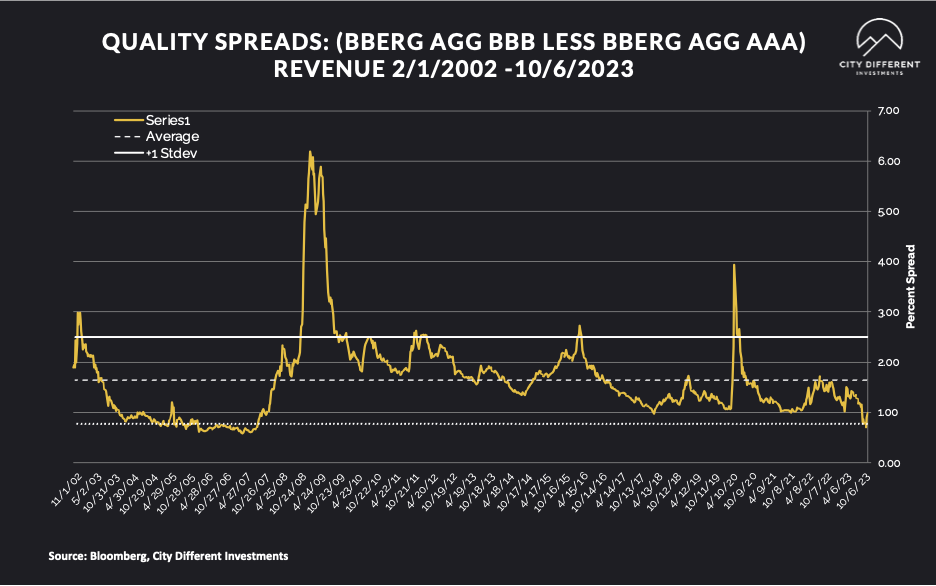

Quality spreads in the taxable market are not attractive but were wider last week, ending the week at 0.99%. High yield quality spreads moved from 3.49 on September 30 to 3.70 on October 6.

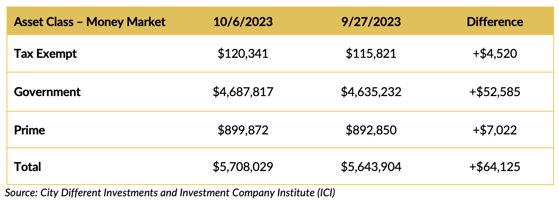

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

In total, money funds saw positive cash flows in all categories. Investors love the yields on money market funds and hate the volatility of bonds funds in a raising yield environment. We feel this type of environment is one in which investors should take prudent risk and not hide from it. Beware the “Cash Trap”.

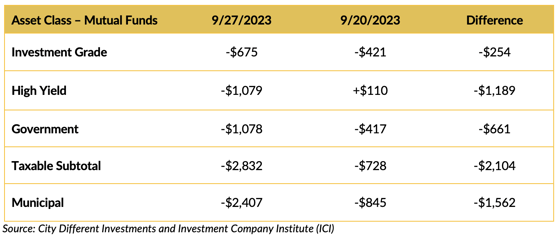

Mutual Fund Flows (millions of dollars)

Bond mutual funds' cash flows were negative across the board.

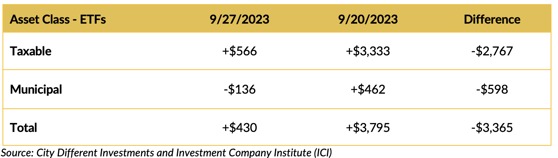

ETF Fund Flows (millions of dollars)

ETF flows were positive last week.

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

This week’s supply estimates are slated for somewhere around $4.5+ billion.

CONCLUSION

The fixed-income markets are looking interesting. The value measures are turning positive. Rather than avoiding risk in money market funds (beware the “Cash Trap”), we think this is a good time for investors to take prudent risk. We plan to use this period to get our SMAs fully invested (in the shorter end of the yield curve) and move our durations up to the top of their respective neutral duration ranges. We would need to see steeper yield curves before we became more aggressive with our market outlook.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.