.png)

WEEK ENDING 10/21/2022

Highlights of the week:

- Possible volatility and insufferable campaign ads mark run-up to midterm elections.

- “Alas, poor United Kingdom! We knew it well.”

- Is a story in The Wall Street Journal from a Federal Reserve plant?

- Municipal bond mutual funds continue to see negative cash flows.

A CITY DIFFERENT TAKE

Last week’s economic calendar gave the Fed no reason to ease up on its fight against inflation. Although an article in The Wall Street Journal titled “Fed Set to Raise Rates by 0.75 Point and Debate Size of Future Hikes” hints that a reduction in interest rate increases (or even a pause) is being debated. That is, of course, after another 0.75% increase at the Fed’s November meeting.

The Fed has been rumored to “socialize” potential changes in policy through stories planted in prominent financial press outlets. Quotes like the following gives one a moment to ponder this rumor.

“Some officials have begun signaling their desire both to slow down the pace of increases soon and to stop raising rates early next year to see how their moves this year are slowing the economy. They want to reduce the risk of causing an unnecessarily sharp slowdown. Others have said it is too soon for those discussions because high inflation is proving to be more persistent and broad.”

In times of higher financial market volatility, market participants come to expect some firm or industry to break due to use of excess leverage. Think real estate during the great recession or a money market fund that breaks the buck. Rarely does a break come in the form of an entire country. Liz Truss’, now the United Kingdom’s shortest-serving prime minister, resignation last week is an example of collateral damage from the Conservative Party’s “growth plan.”

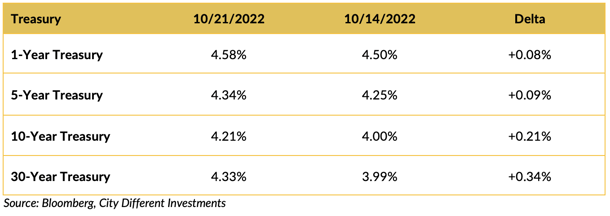

CHANGES IN RATES

Interest rates in the Treasury market moved higher on the week. The long end of the yield curve led the way higher. The Treasury yield curve steepened quite a bit between 1 and 30 years, going from -51 to -25 basis points over the week. Is this an indication that inflation pressures will be more persistent than the market initially thought?

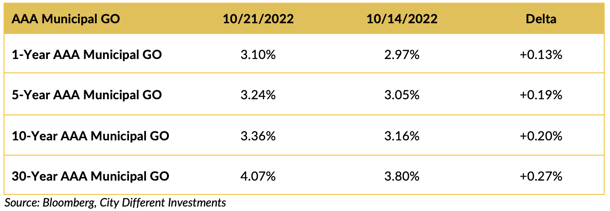

Interest rates in the municipal market increased over the week, but they still have a lot of catching up to do. The municipal yield curve between 1 and 30 years also steepened, moving from 83 to 97 basis points. The municipal market is still lagging behind the Treasury market on both factors (yield change and changes in slope of the curve). One might say that the municipal market is the “lower, slower market”?

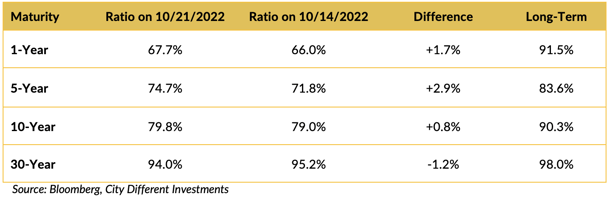

Ratios versus the Treasury market equivalents moved higher over the week, except for the long end of the municipal market, which moved lower.

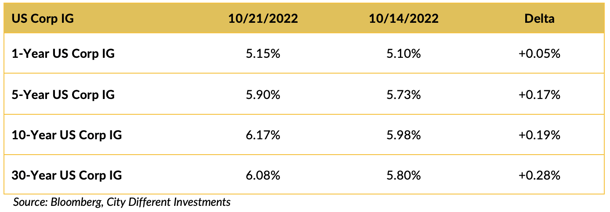

Investment-grade rates marched higher, led by the long end of the yield curve.

THIS WEEK IN WASHINGTON

The midterm elections are only weeks away, and the silly season of campaign ads is in full swing. What’s more annoying, the campaign ads or the Medicare enrollment ads? One makes us want to hide our wallets and the other makes us what to hide our souls.

If the midterms result in a Washington power shift, that could potentially influence U.S. support for the war in Ukraine. An interesting headline from The New York Times which caught our attention last week: “McCarthy Suggests That a G.O.P.-Led House Would Question Aid to Ukraine”.

“The House minority leader, who is in line to be speaker should Republicans win a majority, said in an interview that his party would resist giving a ‘blank check’ to the war-torn country.”

It’s been said that one of Putin’s goals of the invasion of Ukraine was to weaken NATO and the U.S. leadership position in that coalition. We’ll see how the current policy holds post-elections and whether this is a partisan issue that will result in a shift.

Which brings us to recent Jan. 6 committee developments. While we may not all agree with all her policy positions, listening to Rep. Liz Cheney on Sunday’s morning talk shows, it certainly made a statement about her character. A real “Profile in Courage” in the face of overwhelming opposition. In his farewell letter, George Washington warned of the perils of putting political factions above the interest of one’s country. Something that will only increase the division and gridlock present in the current American discourse.

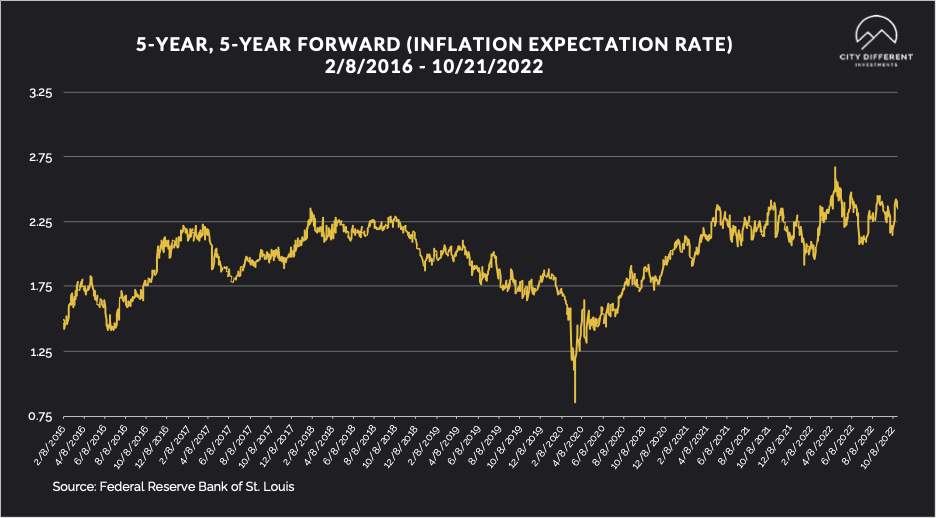

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate ended at 2.35%, 3 basis points lower than the prior week closing at 2.38%. The 10-year Breakeven Inflation Rate ended the week period at 2.52%, 11 basis points higher than the last reported observation of 2.41%. Both of these readings seem low, given where inflation is today.

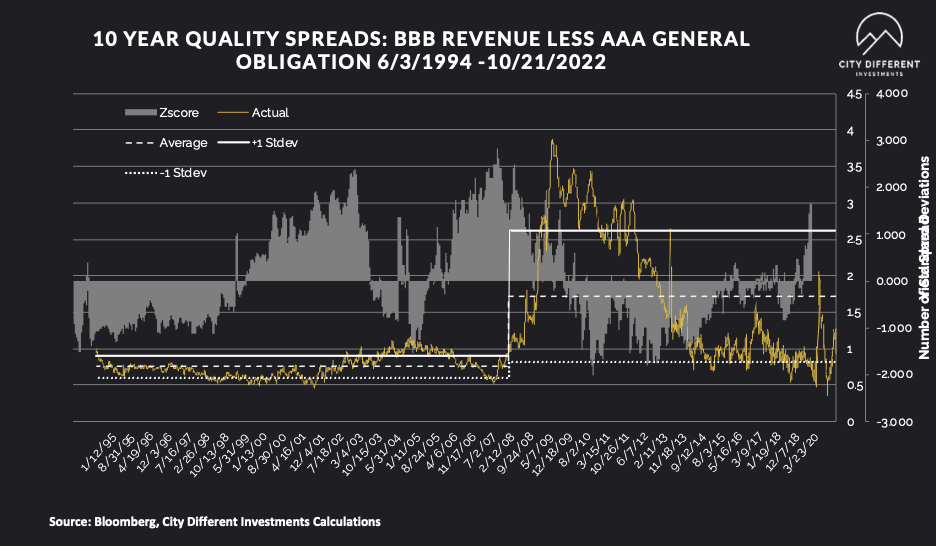

MUNICIPAL CREDIT

Long-term quality spreads continued to widen, moving further into the fair range, and are starting to pique our interest. While we don’t think the move has been significant enough to change our strategic outlook towards credit, it's getting close.

This week's short-term (inside of five years to maturity) quality spreads tightened significantly (15–30 basis points). The question is, why? Is this an aberration in the data, or are market participants moving shorter on the quality curve to limit yield dilution while shortening duration? If it’s the latter, that can be a dangerous game. When a credit goes bad, it doesn’t matter what the maturity is; the price is the same, and usually, the first stop is 50 cents on the dollar.

WHY IS THE MUNICIPAL MARKET BEHAVING THIS WAY?

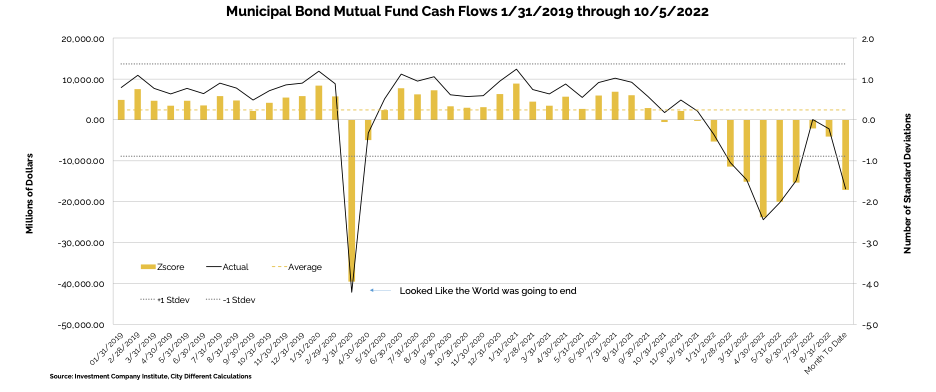

Various sources are used to report cash flows related to municipal bond mutual funds and ETFs, all reporting at different times. The source we have chosen to use is the Investment Company Institute (I.C.I.). The I.C.I. reported weekly cash flows from municipal bond mutual funds for the week of October 12, as -$4.5 billion compared to -$5.2 billion from the week before.

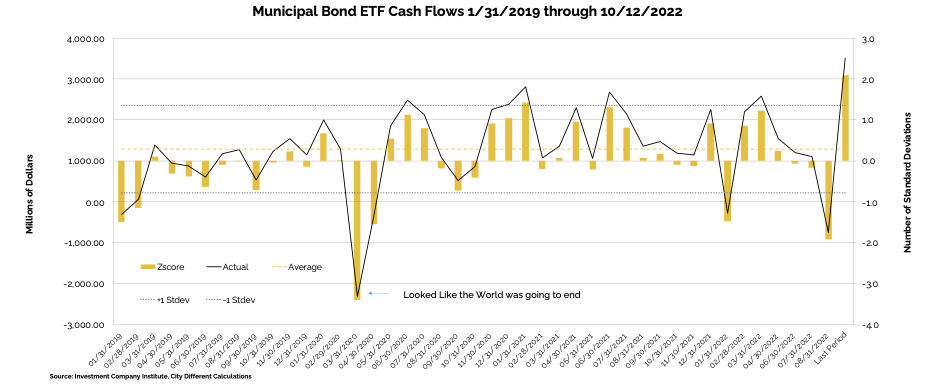

Municipal bond ETF cash flows for the same period were +$2.3 billion, compared to +1.9 million the prior week.

Other cash flow sources:

Lipper reported an 11th consecutive combined weekly and monthly outflow, with $2.6 billion leaving muni funds for the period ending October 19, increased record YTD outflows to $103 billion.

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

In its Municipal Markets Weekly newsletter, JP Morgan commented on the supply picture this week, stating that:

“Next week, we expect total supply of $9.7 billion, or 92% of the 5-year equivalent week average ($10.5 billion). We anticipate tax-exempt supply of $8.9 billion (113% of average), and taxable/corp cusip supply of $0.8 billion (30% of the average).”

The supply picture does not get interesting until it exceeds $10 billion tax-exempt issuances in a given week.

CORPORATE INVESTMENT GRADE AND HIGH YIELD OVERVIEW

In U.S. Investment Grade land, spreads widened slightly to reflect the pushback from the strong US CPI data.

In its weekly "Credit Flows" report, Wells Fargo commented:

“The great un-reach from yield trade. For more than 10 years, investors engaged in a giant reach for yield trade incentivized by super-easy global monetary policies with resulting low global yields and ample liquidity. Central banks fully intended to incite animal spirits with investors being forced to take higher risks in order to enhance returns by creating an environment devoid of yield. Most straightforwardly money flowed down the quality spectrum from government bonds to IG and from IG to HY, thus amplifying spread compression. Now with the pivot toward monetary policy tightening these flows reversed and are moving back up in quality. These investment flows amplify the decompression seen normally in a recession scenario.

Leveraging ample liquidity. But it didn’t stop there - investors were forced to enhance returns in every possible way. For example, many used ample access to leverage to juice returns, as evidenced by the recent experience with UK pensions. This can’t be isolated to UK pensions only but has to be more general to pensions in other countries and most other types of investors. More shoes to drop.

Structure on, structure off. Clearly certain structured products were beneficiaries of the need to take liquidity risk in a low yield environment - including CLOs. The massive CLO bid allowed an erosion of credit quality in the leveraged loan market as the share of B-rated rose to nearly 65% over the last five years from 45%. Clearly that means a higher default rate for leveraged loans in the coming default cycle, which peaking at 8% in the first part of 2024 on an LTM basis we expect to unusually match HY.

Keep things simple. Lower interest rates and ample liquidity via QE fueled the great reach for yield trade. This was the intended consequence of super-easy global monetary policies. Raising interest rates and draining liquidity through QT highlight the shift in markets toward the great un-reach from yield trade. We’re then in the process of learning the longer-term costs of crisis-level monetary policies. In this environment we would keep things simple and buy liquid simple assets - i.e. stick to on-the-run corporate bonds and shy away from using leverage - either outright or structural.

Yields, spreads & returns. Historically there is a very weak relationship between the level of corporate bond yields and future 12-month total return. The level of credit spreads has even less explanatory power for realized excess returns. So while yields are currently high and spreads are wide by historical standards, there is little historical evidence that suggests a sustained mean reversion. CDX meanwhile has a much closer relationship to realized returns from buying protection (short risk).

US IG front end flattening. We are looking for the 5s/10s spread curve to flatten as we expect wider credit spreads and higher Treasury yields. Historically wider spreads lead to flatter 5s/10s spread curves as credit risk takes precedence. 10-year corporates also see demand from yield buyers at higher rates and thus tend to outperform. Moreover, outflows lead to selling where the price impact is least when liquidity comes at a premium.”

CONCLUSION

Expect high volatility in the period leading up to the Fed’s November meeting and the midterm elections. Volatility can be unsettling, but it can also lead to great opportunity if one has the stomach for it. We believe that some of our best investment decisions have also made us the most uncomfortable. Stay safe out there.

.png?width=660&name=signature%20block%20(3).png)

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.