.png)

WEEK ENDING 9/29/2023

- Government shutdown postponed until November 17.

- Will September PCE give Fed a reason to pause?

- September Muni yield backup led to underperformance; current yield attractive.

A CITY DIFFERENT TAKE

On Saturday, President Biden signed a bipartisan spending bill passed by Congress. This funding allows the government to operate until November 17. Congress still has a lot of work to do with regards to the budget. They must pass a yearlong spending bill which includes debt limit discussions. The next priority, however, is an attempt by Rep. Matt Gaetz and other extreme Republicans to remove Speaker Kevin McCarthy.

Moving on to the markets, Friday saw the release of a softer than expected PCE.

In August, PCE rose 0.4% month over month while Core PCE rose by 0.1%. This brings the PCE Index YoY to 3.5% and Core PCE Index YoY to 3.9%. We could see Core PCE (the Fed's favorite inflation measure) undershoot the median projection from the September's Summary of Economic Projections (SEP) which is at 3.7% for year-end core inflation.

Remember, current inflation is higher than the Fed's 2% target. The Fed is going to look for sustained low monthly Core inflation. Trends still support one last rate hike by year’s end, keeping rates high well into 2024.

In September 2023, Bloomberg’s IG Muni index produced a negative monthly total return of -2.93%, marking the lowest monthly return since September of last year (-3.8%) and bringing the 2023 YTD return down to -1.38%. The last two weeks of September saw a massive backup in Muni rates. 10-year municipal yields have surged about 30 basis points according to Bloomberg. We think that municipal yields look attractive now and we advise investors to stay the course and opportunistically add to their municipal allocation.

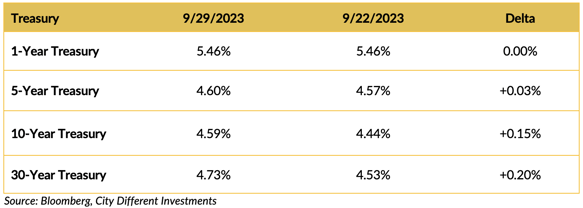

CHANGES IN RATES

Treasury yields were higher on the week. Fear of the Fed’s higher-for-longer policy continues to influence the move to higher yields. The Treasury’s demand for credit (bond issuance) and the potential government shutdown undoubtedly brings into question our ability to govern ourselves. The spread between the 2-year and 10-year Treasury securities was -0.47%, a big move from last week's -0.69%. The yield curve steepened. This could mean recessionary fears are receding and/or possibly long-term inflation fears are rising.

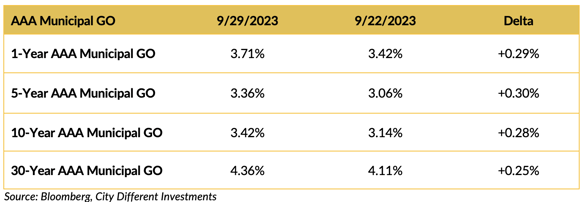

The municipal bond market yields moved higher on the week as well. In addition to the fears engulfing the Treasury market, the municipal bond market has to deal with rising new issuance supply ($8 billion+ next week) and outflows from municipal bond mutual funds (-$17 billion+ YTD).

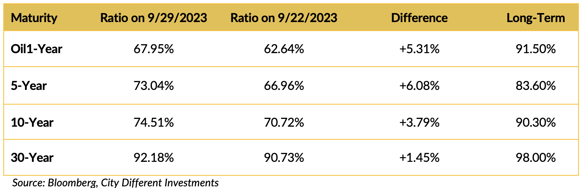

The municipal/Treasury ratios cheapen across the board, as the municipal market adjusts to the unique challenges it faces.

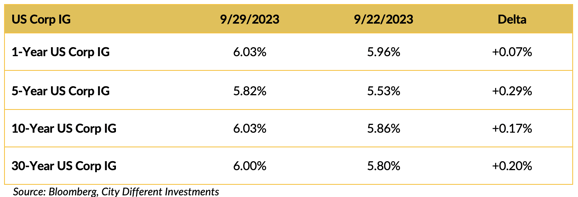

Corporate yields moved higher last week.

THIS WEEK IN WASHINGTON

.png?width=1920&name=graphs%20in%20order%20(1).png)

After the passage of the temporary spending bill, the biggest headline in Washington is the possible removal of House Speaker Kevin McCarthy. Leading the charge to remove McCarthy is Rep. Matt Gaetz (R–FL). Gaetz would need wider support to boot out McCarthy, who currently has help from the Democrats. If Gaetz fails in his attempt, it would reveal that he and his base are marginal in the Republican party. In any case, we will see another round of Republican brinkmanship.

Polarization in politics almost cost us a government shutdown. For now, however, the can has been kicked down the road to November.

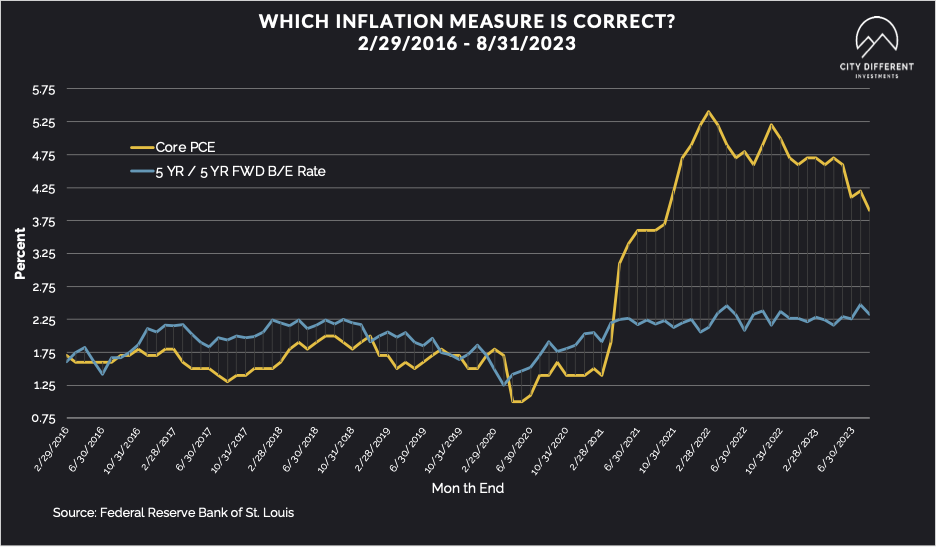

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Break-even Inflation Rate finished the week at 2.48%, three basis points higher than the September 22 close of 2.45%. The 10-year Break-even Inflation Rate finished the week at 2.35%, two basis points lower than the September 22 close.

We wrote about this topic last week and think it bears repeating. This will be the last week we include it.

Is the 5-year Break-even inflation rate worth anything?

We have noted the difference between this measure and Core PCE for some time. The 5-year Breakeven Inflation Rate is the market’s current estimate of the average inflation rate for the next five years. We took some time to look at this measure for the periods from 2/16/2016 through 8/31/2018. This is a small sample, but it is all we have. The average difference between this measure and the 5-year average Core PCE measure is 0.23%. The maximum difference is 0.76%. And the minimum difference is -0.28%. The standard deviation of this analysis is 0.32%.

Our analysis is the sample size is too small to judge, but the 5-year Breakeven Inflation Rate’s value as an inflation forecast (unless used for hedging calculations) is suspect.

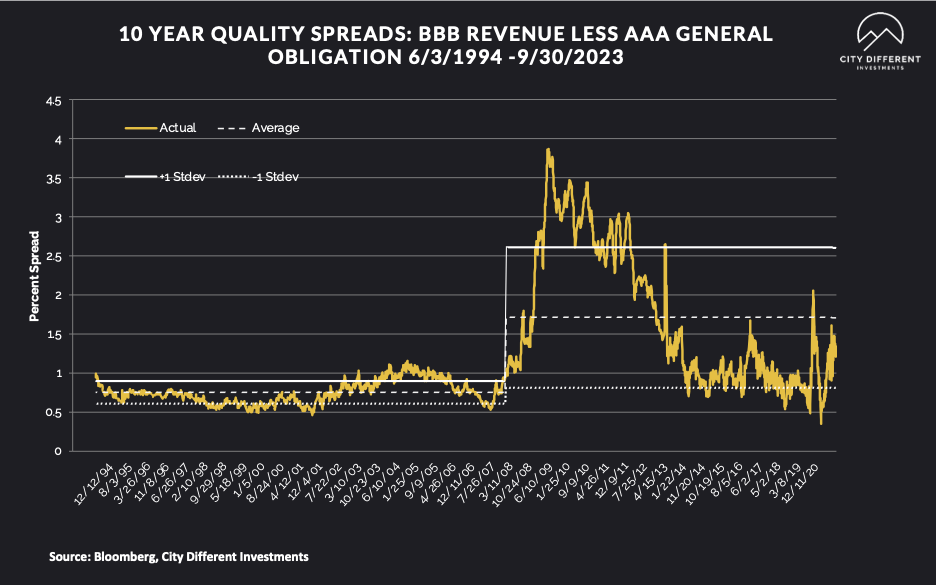

MUNICIPAL CREDIT

10-year quality spreads (AAA vs. BBB) as of September 30 was 1.26%, five basis points higher from the September 22 reading of 1.21% (based on our calculations). The long-term average is 1.71%. By our way of thinking, we still think lower-quality securities are not attractive. Municipal market credit spreads usually take a little more to adjust, given a significant baseline market revaluation.

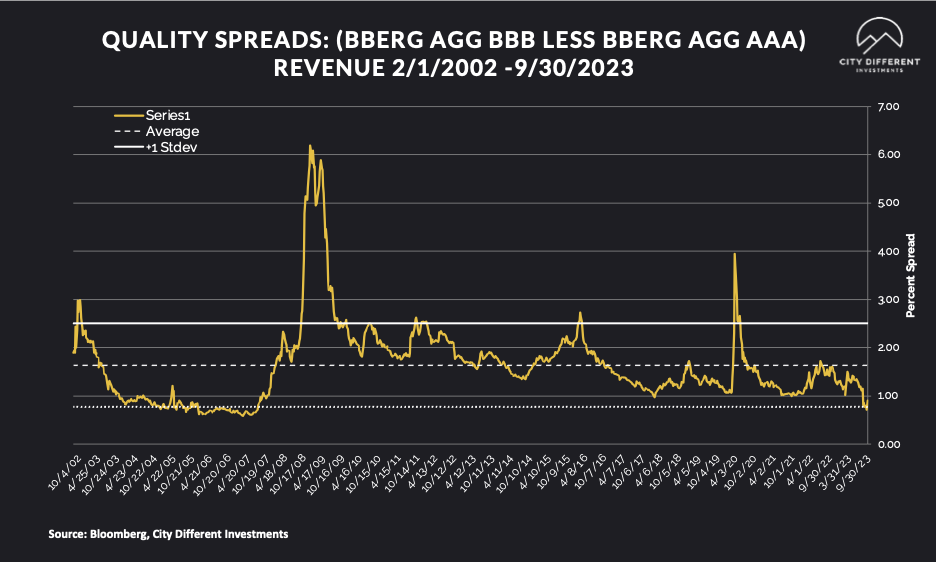

Quality spreads in the taxable market are not attractive but were wider last week, ending the week at 0.90%.

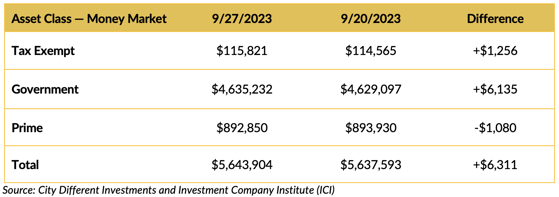

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

Money funds, in total, saw positive cash flows across two of the three subcategories last week.

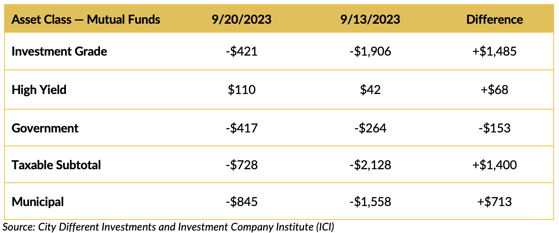

Mutual Fund Flows (millions of dollars)

Bond mutual funds' cash flows were mixed.

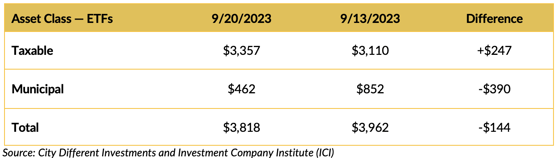

ETF Fund Flows (millions of dollars)

ETF flows were positive last week.

SUPPLY OF NEW ISSUE MUNICIPAL BONDS

This week’s supply estimates are slated for somewhere around $8 billion+.

CONCLUSION

The country needs a yearlong spending bill. A government shutdown has been averted until November 17 while Speaker McCarthy's future as leader is uncertain.

Softer Core PCE shows the Federal Reserve is making progress against its fight against inflation. Massive yield backup in municipal rates have led to market underperformance. But we urge investors to stay the course and opportunistically add to their municipal allocation.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein are available upon request.