Municipal bond investors are spending a lot of time talking about taxes. They worry the Manchin and Sanders wings in Congress will finally reach a compromise on the infrastructure and reconciliation bills, sending taxes higher. Others still hope tight majorities and an even tighter legislative calendar will scuttle the whole program.

That debate misses the point. Regardless of what happens on the Hill, rising taxes aren’t the only risk to consider in judging evaluating municipal bonds. In fact, I’d argue taxes are the least important risk. If muni bond investors are looking for something to fret about, they have a long list of worries to choose from. Here are the top six:

- Credit risk

- Duration risk

- Yield curve risk

- Prepayment risk

- Reinvestment risk

- Taxability risk (“Bob Packwood” risk)

For the moment, investors seem happy to overlook all those considerations, as they pile into municipal bonds seeking a low-risk hedge against tax hikes. Up until recently, the demand for tax exempt municipal bonds has been insatiable in 2021. Cash flows YTD into municipal bond mutual funds, as measured by the Investment Company Institute, exceed $76B through 9/29/20211. Cash flows into municipal bond ETFs (the mutual funds’ younger siblings) reached $16B for the same period2. These inflows have caused a supply-demand imbalance which has lessened the assets’ relative value—and exacerbated some of the risks mentioned above. This imbalance reached $50B at the end of August 2021, based on analysis provided by Siebert Williams Shank & Co LLC. It is a classic example of too much money chasing too few assets. Never a good combination for a portfolio manager whose decision-making process is based, in part, on relative value metrics. As the relative value of the security or asset class declines the relative risk of those assets increases. When that happens a total return manager will take on less risk (duration, credit or other) because they are not being paid enough to make it worthwhile.

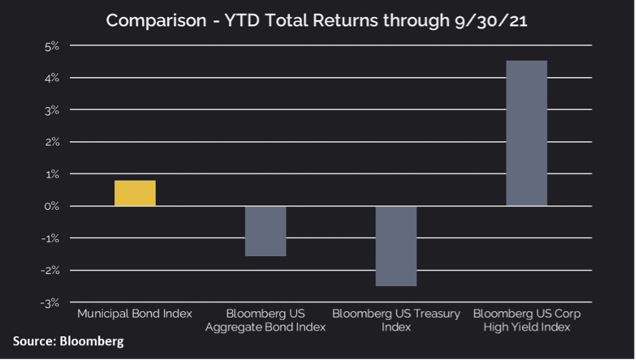

Adding to the attractiveness of the asset class, the municipal bond market has performed well this year, posting a YTD total return of 0.79%. This compares very favorably to the Bloomberg US Aggregate Bond Index’s total return of -1.55% and the Bloomberg US Treasury Index’s total return of -2.50%, although not as impressive as the Bloomberg US Corporate High Yield Index’s 4.53%.

All markets are driven by two factors: fear and greed. Currently, greed is in charge. The ultra-accommodative fiscal policy adopted by the Federal Reserve since the onset of the pandemic has made it impossible for investors to generate adequate levels of income without taking on more and more risk. The urge to pursue income regardless of risk—greed—can become a big problem when the music stops, and fear starts to take hold. Investors who blindly grab at every tax-exempt muni offering now may eventually come to regret it.

Taxes might rise. Taxes might not. In any case, this is no time to make an investment decision based on only one risk factor, and a highly uncertain risk factor at that.

Subscribe to the City Different Investments blog to join in our ongoing discussion of the market and other timely topics.

1 https://www.ici.org/research/stats/weekly-mfflows

2 https://www.ici.org/research/stats/weekly-etf