“Don't fight the Fed” — it’s an adage for a reason, and it’s one we believe in. Why? Because history has mostly demonstrated the Federal Reserve, with its monetary policy tools, is overwhelmingly more powerful (and more informed) than market participants.

.png?width=900&height=300&name=Penalty%20Kicks%20(1).png)

But bad things can happen to investors when they try to read the Fed’s tea leaves instead of actually listening to what the Fed is telling them.

A short while ago (December 2023 to be exact), the markets predicted a combination of lower inflation and slowing economy would produce 6 rate cuts in 2024. Even though the Fed was publicly saying it would likely only cut rates three times in 2024, large sectors of the market heard “six.” Fast forward three months, and after some strong economic news (and well-reasoned Fed Speak), it appears that there is a low probability of a rate cut in March and perhaps as few as 3 rate cuts this year.

The bottom line is that it’s really hard to predict with any certainty or accuracy when the Fed will move, and by how much. And given that fixed income portfolios are especially sensitive to interest rate changes, you can end up taking on far too much duration risk based solely on bullish prognostications (that are at odds with the Fed’s own messaging to boot).

At City Different, we are total return investors. That means we take risk when we’re paid to take risk. In a fixed income portfolio, a major type of risk is duration risk. In simple terms, it means how price sensitive is a portfolio to interest rate changes. We break down our duration risks into three segments:

- Bearish: low duration risk

- Neutral: akin to Goldilocks finding the right porridge — it’s just right, and you wouldn’t/shouldn’t leave this zone unless there’s very compelling evidence to nudge you one way or the other

- Bullish: higher duration risk

We position our portfolios in response to macro-economic trends to be sure, but strategically, we’re positioned in the neutral range about 67% of the time, whereas we’ll be bearish or bullish about 16.5% of the time each, respectively.

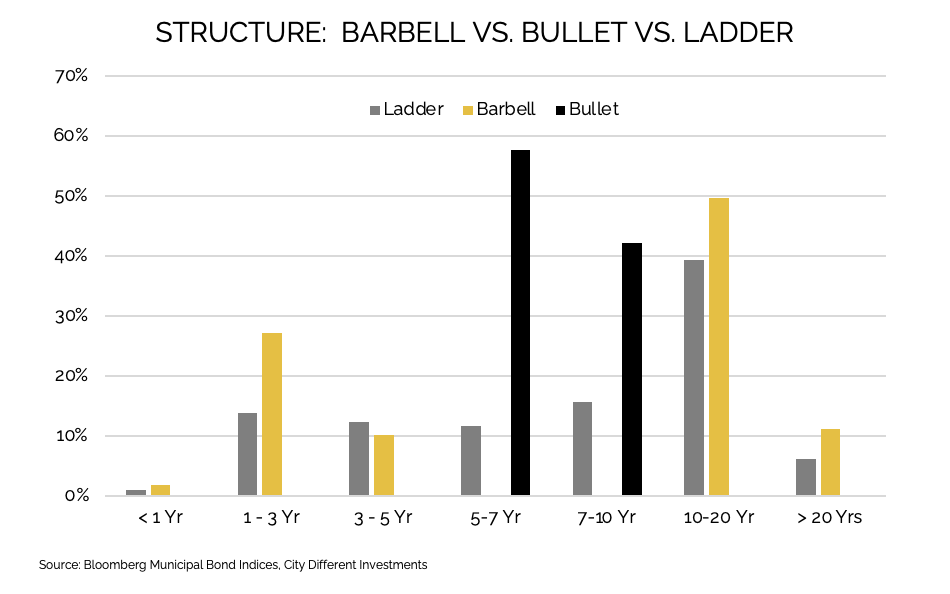

We accomplish our portfolio duration targets by utilizing a laddered structure. Using municipal bonds as an example, historically, a laddered structure outperforms1 the two other most common structures (bullet and barbell) 60% to 80% of the time (with lower turnover and reinvestment risk).

1Outperformance is defined as an excess of total return when compared to bullet and barbell bond investment strategies over the period December 2011 through December 2023.

1Outperformance is defined as an excess of total return when compared to bullet and barbell bond investment strategies over the period December 2011 through December 2023.

This might seem pretty simple, but sometimes the simplest things are often overlooked.

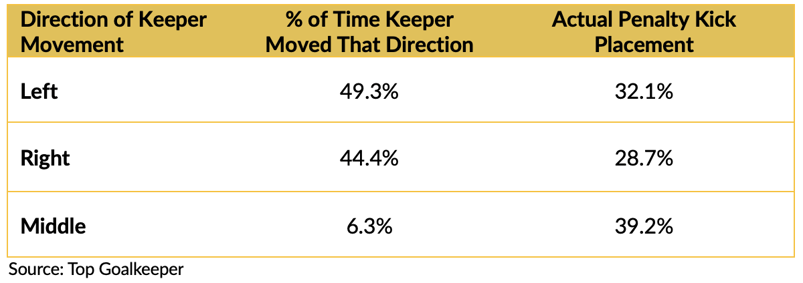

You can see examples of this in a non-investment context as well. Much as market anticipation is the name of the game when calculating duration risks, anticipation is also the hallmark of a goalkeeper’s approach to a penalty kick in soccer.

At least, you’d think it was.

But contrary to popular belief, it actually isn’t. The following table from Top Goalkeeper (citing this study) illustrates this:

The penalty kick actually comes down the middle more than it goes to either side, but the goalie only stays put about ~6% of the time… a huge behavioral inefficiency based on the underlying statistics. The same is true of bullish and bearish fixed income portfolios — we position ourselves there in narrow bands because we’re far less likely to actually experience those conditions.

The real key to both penalty saves and fixed-income portfolios is having a disciplined and well-tested philosophy… and sticking to it.

IMPORTANT DISCLOSURES

The information and statistics contained in this communication have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or forecasts discussed herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice. Please remember that past performance may not be indicative of future results.

Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product, or any non-investment related content, made reference to directly or indirectly in this communication will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. No discussion or information contained herein serves as the provision of, or as a substitute for, personalized investment advice. To the extent that a reader has any questions regarding the applicability above to his/her individual situation of any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal, tax, or accounting advice.

Opinions and statements of financial market trends that are based on market conditions constitute our judgment and are subject to change without notice. Historic market trends are not reliable indicators of actual future market behavior. This material may contain projections or other forward-looking statements regarding future events, targets or expectations, and is only current as of the date indicated. There is no assurance that such events or targets will be achieved and may be significantly different than that shown here. The information presented, including statements concerning financial market trends, is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Although the assumptions underlying the forward-looking statements that may be contained herein are believed to be reasonable, they can be affected by inaccurate assumptions or by known or unknown risks and uncertainties. The Firm assumes no duty to provide updates to any analysis contained herein.