Last week, the Fed announced that it would not raise the Fed Funds rate in September. By our way of thinking, though, they left the door open for future increases (data dependent). This left us pondering whether the current Fed Funds Rate is restrictive or not (we think that many of the talking heads are suffering from recency bias, or we may be just data mining). What follows is our attempt to answer this question (a word of caution, though — a limitation of this analysis is the available data. We think we have enough, but others may disagree).

Step One:

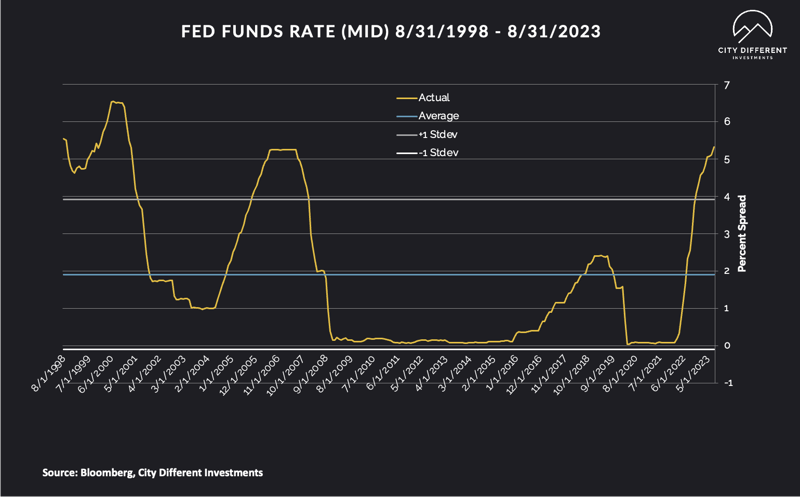

Let’s look at the raw and Feds Rate from 8/31/1998 through 8/31/2023. We measure the degree of restrictiveness by how many standard deviations the current Fed Funds rate exceed the long-term mean. As of 8/31/2023, the current Fed Funds rate is 1.7 standard deviations above its long-term mean. The following graph illustrates this measure:

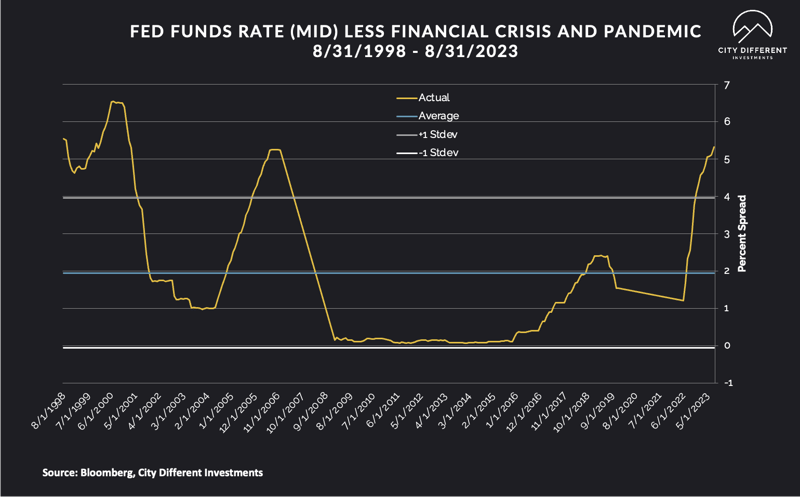

There are two periods when the Fed Funds rate was at or near zero: the 2007-2008 financial crisis and the 2020-2023 pandemic. These periods were defined by existential threats to the economy during each respective crisis. If we exclude most of those periods and recalculate, the nominal Fed Funds rate looks restrictive. See the graph below:

Step Two:

Step Two:

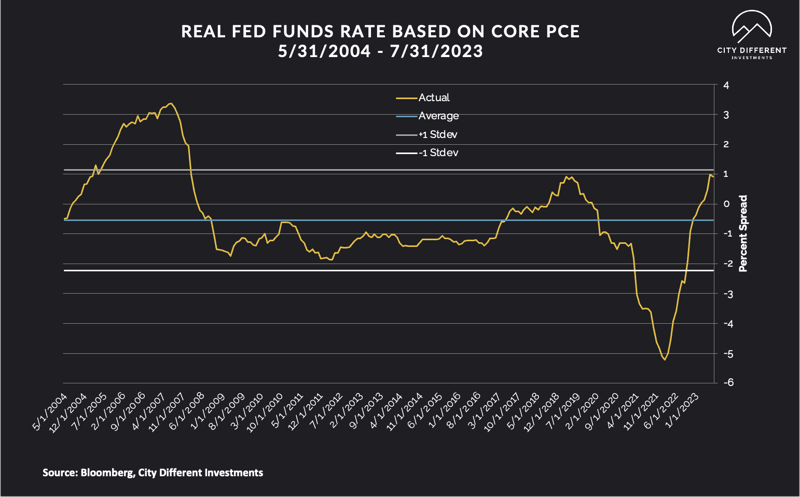

This type of analysis is not enough because we need to adjust for inflation (since Core PCE is the Fed's favorite inflation measure, we will use that as our inflation adjustment).

The following graph shows the real Feds Funds rate (nominal Fed Funds Rate Less Core PCE) for the entire period from 5/31/2004 through 7/31/2023. Based on our calculations, the real Fed Funds rate is 0.87 standard deviations higher than the long-term mean. This indicates that the real Fed Funds rate is not yet in restrictive territory, but it is getting close.

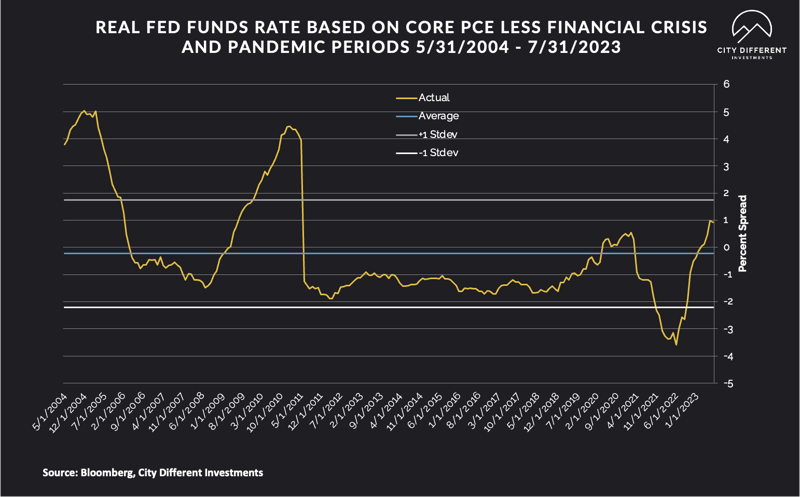

What happens if we make the same time adjustments for the financial crisis and the pandemic? Think of it this way: out with the new normal, welcome to the old normal.

The conclusion is the same — this adjusted real Fed funds rate is 0.58 standard deviations higher than the long-term average, which means the Fed is less restrictive than we initially thought.

Conclusion:

Higher for longer seems to be the correct policy outcome (assuming the Fed does not break anything — think Silicon Valley Bank — and inflation stays stubbornly above the Fed’s 2% target). The last ten or so years were filled with two major existential economic threats; we think those were the anomalies. The upside for investors is that fixed income securities are valuable even if rates increase slightly from here. Here is an example of that thought process in action:

Type of Strategy: City Different Investment’s Limited Term Municipal Composite SMA

Beginning Date: 8/31/2021

Option Adjusted Duration: 2.17 years.

Average Gross Yield: 0.48%

Yield Delta: +0.25%

Price loss: 0.54%

Months of income lost: 13.5 months.

Beginning Date: 9/20/2023

Option Adjusted Duration: 3.14 years.

Average Gross Yield: 3.25%

Yield Delta: +0.25%

Price loss: 0.79%

Months of income lost: 2.91 months.

Given these measures, we believe investors should think about a laddered Limited-Term SMA:

- The value proposition is interesting

- They protect themselves from the risk of a cash trap

- Even if rates increase from here, an actively managed, laddered portfolio will be able to benefit as securities mature and the proceeds are reinvested at higher rates

- If interest rates move lower from here, an actively managed, laddered portfolio provides the investor with a durable dividend stream

Long-term investors should only take reasonable risks when the return dynamics are in their favor. Many investment managers’ careers have faltered when trying to predict the bottom of markets — if you wait until it’s the perfect time, you lose it. We see the current risk/return dynamics in the fixed-income markets as favoring long-term investors. We also see an actively-managed, laddered portfolio as the best strategy to ensure long-term success.

If you have any questions, please get in touch with Sweta or me!

IMPORTANT DISCLOSURES

The information and statistics contained in this communication have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or forecasts discussed herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice. Please remember that past performance may not be indicative of future results.

The objective of the Limited-Term Municipal strategy is to maximize a sustainable dividend stream while minimizing volatility through a long-term, tax-efficient total return approach. Maturities range between 1-10 years, with a midpoint neutral duration target of 3.5 years. Portfolios invest primarily in tax-exempt municipal bonds utilizing a laddered structure. Taxable municipal bonds and municipal investment vehicles may also be eligible if relative value and risk parameters permit. Investments are limited to those with investment-grade ratings at time of purchase. An investment in the strategy is subject to certain risks. While income from investing in municipal bonds is generally exempt from Federal and state taxes for residents of the issuing state, income from municipal bonds may at times be subject to state and local taxes and/or the alternative minimum tax. The value of an investment, and income generated (if any) may fall as well as rise and is not guaranteed. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product, or any non-investment related content, made reference to directly or indirectly in this communication will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. No discussion or information contained herein serves as the provision of, or as a substitute for, personalized investment advice. To the extent that a reader has any questions regarding the applicability above to his/her individual situation of any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal, tax, or accounting advice.Opinions and statements of financial market trends that are based on market conditions constitute our judgment and are subject to change without notice. Historic market trends are not reliable indicators of actual future market behavior. This material may contain projections or other forward-looking statements regarding future events, targets or expectations, and is only current as of the date indicated. There is no assurance that such events or targets will be achieved and may be significantly different than that shown here. The information presented, including statements concerning financial market trends, is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Although the assumptions underlying the forward-looking statements that may be contained herein are believed to be reasonable, they can be affected by inaccurate assumptions or by known or unknown risks and uncertainties. The Firm assumes no duty to provide updates to any analysis contained herein.