.png)

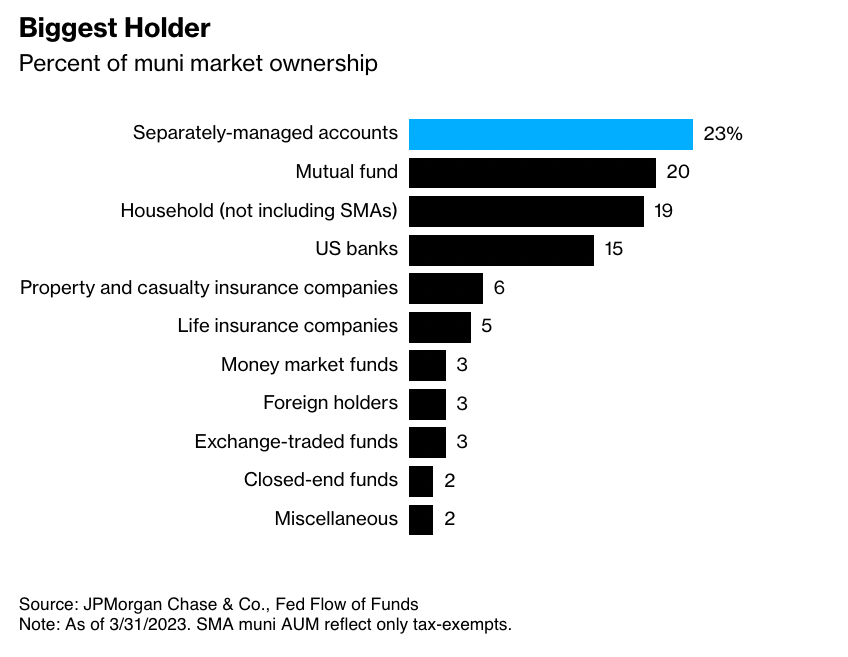

Separately Managed Accounts (SMAs) have grown from 3% of the total Municipal Market to approximately 23% market share in the last decade (as of 3/31/2023). Mutual funds, on the other hand, make up around 20% of market share, with ETFs coming in at 3%. In other words, SMAs have displaced mutual funds as the largest share of the municipal market, with nearly $1 trillion in total assets under management. Which raises the question — why has so much municipal money flowed into SMAs in the last ten years?

Before we answer that question, let’s take a step back to better understand what exactly an SMA is in the first place.

We like the Wall Street Journal’s definition: SMAs let you directly own individual stocks, bonds and/or other assets instead of buying a one-size-fits-all investment pool (like a mutual fund or ETF). The primary goals are to offer account holders greater upside potential and more tax flexibility than mutual funds or ETFs can provide (for more in-depth analysis on why SMAs can provide that, check out our blog post here).

So why has this investment vehicle grown so much (more specifically in the tax-exempt municipal market)?

SMAs have captured much of the outflow from mutual funds for a number of reasons. Investors like the individual attention to their goals and risk appetites SMAs afford. Mutual funds or commingled vehicles do not offer this level of control on any investment decision.

The personalization that comes with an SMA is extremely attractive to investors who also cannot control capital-gains distributions in a mutual fund. In a separately managed account, investors can continuously manage for tax loss harvesting. Simply put, you can harvest your losses throughout the year to your advantage (another feature that is customized to the portfolio and the investors’ criteria). Clients can also limit losses via state preferences (e.g., for clients in high-tax states like CA, MA, etc.).

The customization that SMAs provide allows portfolio managers to cater to individual tax situations and attempt to maximize returns on an after-tax basis for clients. Customization can also extend to credit quality and duration.

SMAs can also provide increased transparency — investors can see credit and duration bets (among other risk vectors) that drive portfolio performance in their individual accounts; this empowers them to understand their investments better.

SMAs protect investors from a herd mentality. In funds, positive or negative news can spur inflows and outflows to investors’ possible detriment.

As you can see, there are a host of reasons to consider SMAs (clearly, given how much municipal market money has flowed into SMAs out of mutual funds). But the icing on the cake? From our experience, SMAs are generally priced competitively to their mutual fund counterparts. Given the flexibility, transparency, personalization, and risk protection offered by SMAs, it makes sense that this investment vehicle is attracting more and more interest.

IMPORTANT DISCLOSURES

The information and statistics contained in this communication have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or forecasts discussed herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice. Please remember that past performance may not be indicative of future results.

Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product, or any non-investment related content, made reference to directly or indirectly in this communication will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. No discussion or information contained herein serves as the provision of, or as a substitute for, personalized investment advice. To the extent that a reader has any questions regarding the applicability above to his/her individual situation of any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal, tax, or accounting advice.

Opinions and statements of financial market trends that are based on market conditions constitute our judgment and are subject to change without notice. Historic market trends are not reliable indicators of actual future market behavior. There are additional differences between separate accounts and mutual funds that have not been outlined herein. A mutual fund’s prospectus includes investment objectives, risks, fees, expenses, and other information that should be read and considered carefully before investing.