.png)

WEEK ENDING 2/13/2026

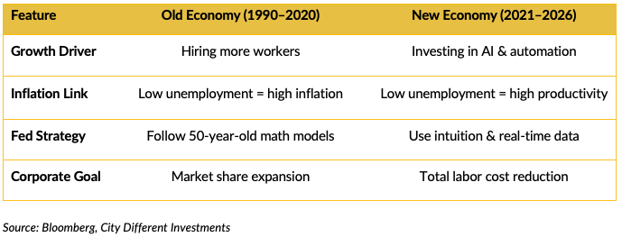

- Jobs Gap: After massive updates, “strong” economy appears to be built on shaky foundation.

- Automation Rules: Big companies are producing more with fewer people.

- Old School: Fed needs to revamp its pre-AI toolkit and models.

A CITY DIFFERENT TAKE

The January economic data paints a picture of a resilient yet recalibrated labor market. A “solid” gain of 172,000 private jobs and a dip in the unemployment rate to 4.3% have effectively quieted immediate recession alarms, despite massive benchmark revisions slashing nearly one million jobs from previous years.

While the employment report surprised to the upside, December’s flat retail sales suggest consumers are finally tightening their belts to rebuild savings, which now sit at a three-year low of 3.3%. On the inflation front, the January Core CPI rose a “mildly dovish” 0.30%, bringing the year-over-year pace to a cycle-low of 2.5% and signaling that while price pressures remain firm — particularly in super-core services — the feared re-acceleration hasn't materialized.

The economy has undergone a massive shift since the pandemic, moving away from a traditional “hiring and spending” model toward one driven by technology. Companies are now laser-focused on cutting labor costs through automation. This means that while the economy is still growing, it no longer needs to hire millions of people to do so. In fact, we are seeing solid growth even though job gains are nearly flat, a trend that completely flips old economic rules on their head.

The Federal Reserve is currently in a difficult spot because its “instruction manuals” — the mathematical models they use to predict the future — are broken. These models traditionally assume that if people have jobs, inflation will go up. However, because companies are using AI and new technology to be more efficient, they can keep prices steady even when the labor market is tight. If the Fed ignores this “productivity boom” and keeps interest rates too high, it risks causing a recession by accident.

For regular investors and savers, this means the higher-for-longer era of interest rates might be ending sooner than the experts admit. The massive downward revisions in job data suggest the economy isn't overheating at all; it’s actually cooling down quite rapidly. When the government eventually admits the labor market is weak, we expect interest rates to fall, which typically causes bond prices to rise.

Looking ahead to the rest of 2026, the big question is whether the Fed will trust its intuition or stick to its old formulas. The current data shows that while prices for things like housing and services are still a bit high, the underlying engine of the economy is slowing down. We are watching for a shift in leadership at the Fed that might prioritize real-time data over 30-year-old theories, which would be the final signal that the economic “rules of the road” have permanently changed.

CHANGES IN RATES

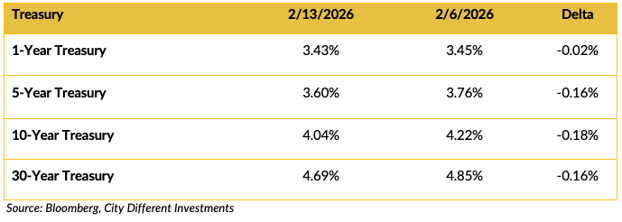

TreasuryMarket

The Treasury market rallied, due primarily to two big pieces of data:

· Cooling Inflation: Consumer Price Index (CPI) data showed inflation slowed to 2.4% year-over-year, down from 2.7% in December. This “soft” report gave investors hope that the Fed would have more room to cut interest rates later in the year.

· Mixed Jobs Data: Earlier in the week, a report showed the U.S. added 130,000 jobs in January. While this was “stronger than expected” (beating estimates of 65,000), it was seen as a “moderate” or “stabilizing” figure that wouldn't necessarily force the Fed to keep rates high forever.

The 2-year yield fell to 2022 levels, and the 10-year fell to Nov. 2025. The 2/10 spread moved down by 10 basis points, lower than last week (0.74% vs. 0.64%).

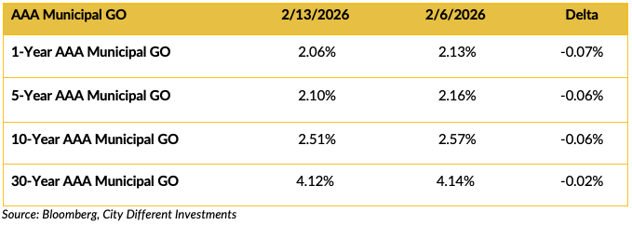

Municipal Market

The municipal market rallied, too. However, the magnitude is lower than the Treasury market. The 2/10 spread for last week is at 46 basis points and has been bouncing around since the beginning of the year.

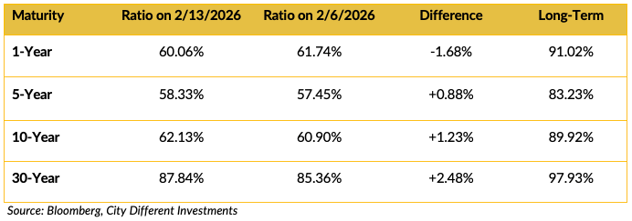

Selected Municipal AAA General Obligation Bond / Selected Treasury Bonds Yield Ratio

Treasury-muni ratios tightened in 1-year tenor and widened slightly in the longer parts of the yield curve.

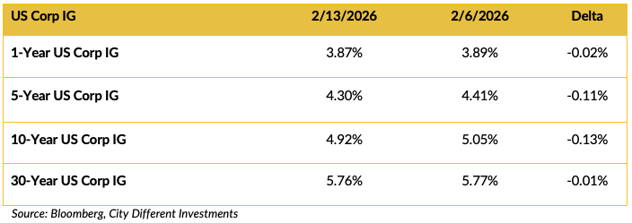

Investment Grade Corporates

Investment-grade corporate bond yields were marginally lower week over week and did not follow the Treasury market.

THIS WEEK IN WASHINGTON

The path for Kevin Warsh (President Trump's pick to replace Jerome Powell as Fed Chair in May) has hit a major roadblock. Senator Thom Tillis (R-NC) is currently blocking all Fed nominations until the DOJ resolves its investigation into Chair Powell's role in the Fed building renovation costs. This creates a scenario where Powell could remain as acting chair indefinitely after his term expires. Market analysts are closely watching the “Warsh Tension.” Warsh is a vocal critic of the Fed's $6.6 trillion bond portfolio. If he is eventually confirmed and moves to shrink the balance sheet, it could push mortgage rates higher, directly clashing with President Trump's campaign promise to lower housing costs.

Since the Bureau of Labor Statistics (BLS) is partially affected by the shutdown, investors are bracing for potential delays in economic data. However, the delayed Q4 GDP report is still expected to land next week with a 3.0% forecast, which will be the ultimate “vibe check” for the economy. Congress is currently in a 10-day recess for the holiday. While this provides a breather, it also means the DHS shutdown will likely persist until lawmakers return to D.C. to negotiate a path forward.

With the 2026 midterms approaching, expect more “America First” executive actions. Last week saw orders on Arms Transfer Strategies and Clean Coal; more orders are rumored for this week as the administration seeks to bypass a stalled Congress.

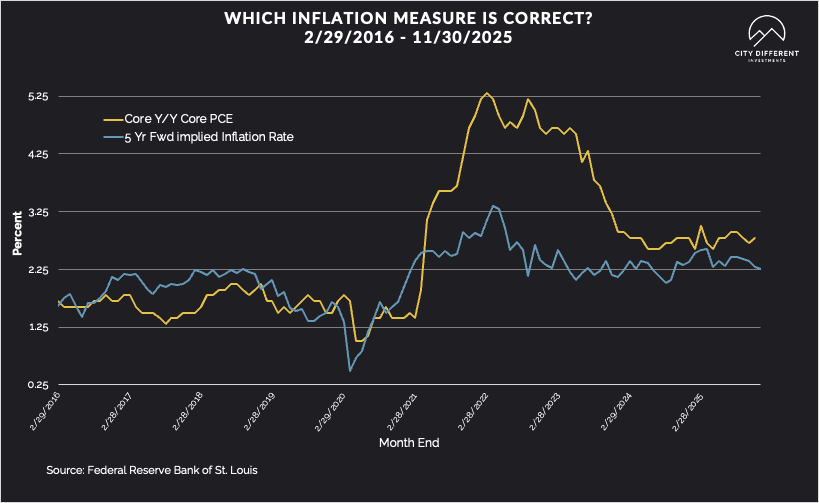

WHAT, ME WORRY ABOUT INFLATION?

The 5-year Breakeven Inflation Rate finished the week of Feb. 12 at 2.45%, 5 basis points higher than last week. The 10-year Breakeven Inflation Rate finished the period at 2.29%, 5 basis points lower than last week.

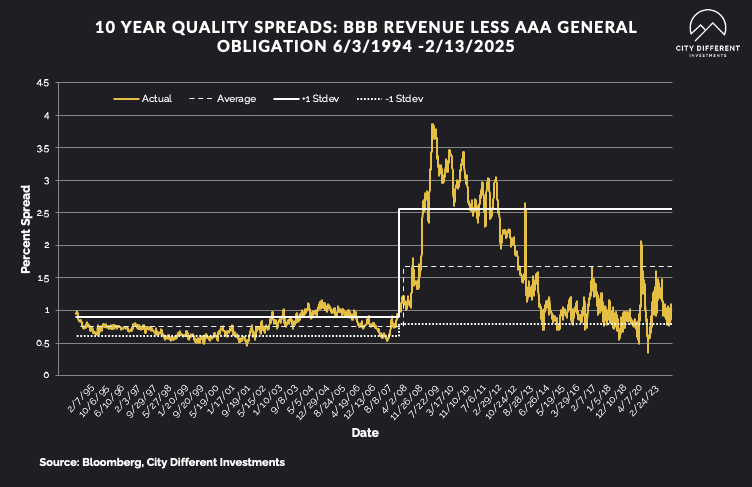

MUNICIPAL CREDIT

Last week's 10-year quality credit spread between BBB revenue bonds and AAA general obligation bonds was lower by 2 basis points for the week at 0.89%. The historical average credit spread is at 1.68%.

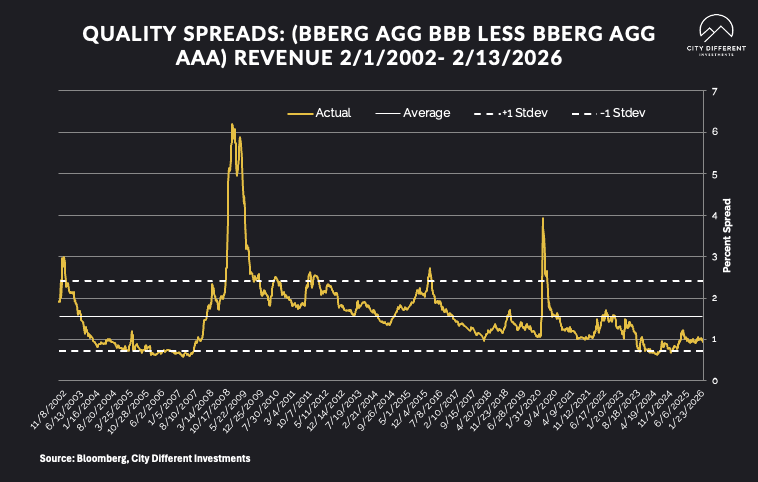

TAXABLE CREDIT

Investment-grade spreads are tight at 59 basis points this week. Credit spreads materially converged last week. The long-term average is 1.56%.

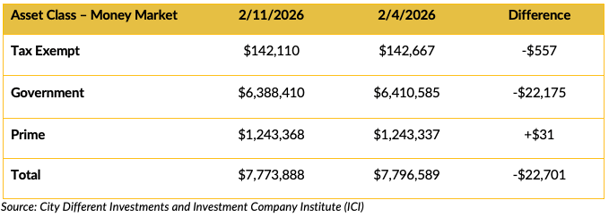

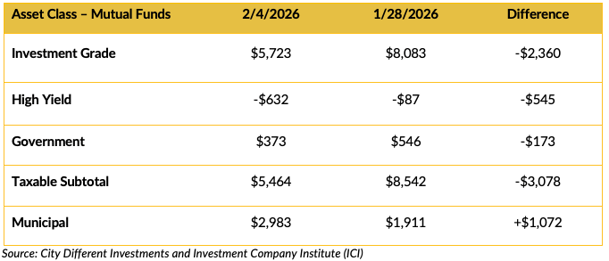

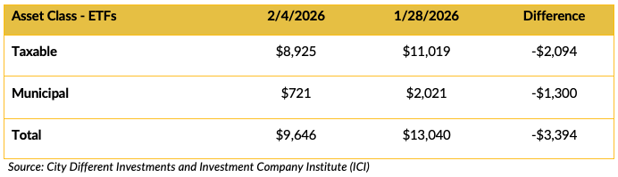

WHERE ARE FIXED-INCOME INVESTORS PUTTING THEIR CASH?

Money Market Flows (millions of dollars)

Money market fund flows were largely higher week-over-week.

Mutual Fund Flows (millions of dollars)

Mutual fund flows were mixed for last week.

ETF Fund Flows (millions of dollars)

Net ETF flows were weak, down in all categories.

SUPPLY OF NEW ISSUE BONDS

Looking ahead to the second half of February, the market is set to receive a massive $19 billion infusion of reinvestment capital (from maturing bonds and coupon payments), which, combined with a “flight to quality” rally in U.S. Treasurys, is expected to keep liquidity strong. Despite a steady stream of new deals — including an expected $6.7 billion in tax-exempt issuance next week — demand remains robust.

CONCLUSION

The current economic landscape represents a fundamental decoupling of growth from labor, rendering traditional metrics like the Phillips Curve — which historically linked employment levels to inflation — increasingly obsolete. As AI and automation allow corporations to scale productivity without expanding headcounts, the “Jobs Gap” serves as a stark warning that the old instruction manuals used by the Federal Reserve may be steering the ship toward an unnecessary recession. Navigating the rest of 2026 will require a pivotal shift in strategy; for the economy to remain resilient, policymakers and investors must look past lagging employment data and embrace a new reality where efficiency, rather than hiring, is the primary engine of value.

IMPORTANT DISCLOSURES

The information and statistics contained in this report have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks or estimates presented herein are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks or assumptions should not be construed to be indicative of the actual events which will occur. These projections, market outlooks or estimates are subject to change without notice.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product or any non-investment related content, made reference to directly or indirectly herein will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions.

All indexes are unmanaged, and you cannot invest directly in an index. Index returns do not include fees or expenses. Actual portfolio returns may vary due to the timing of portfolio inception and/or investor-imposed restrictions or guidelines. Actual investor portfolio returns would be reduced by any applicable investment advisory fees and other expenses incurred in the management of an advisory account.

You should not assume that any discussion or information contained herein serves as the receipt of, or as a substitute for, personalized investment advice from City Different Investments. To the extent that a reader has any questions regarding the applicability above to his/her individual situation or any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm and no portion of this content should be construed as legal or accounting advice.

A copy of City Different Investments' current written disclosure statement discussing our advisory services and fees is available for review upon request.

Unless otherwise noted, City Different Investments is the source of information presented herein.

A description of the indices mentioned herein is available upon request.