It’s probably time to worry about inflation for real. But as someone who’s run two bond desks (Thornburg and Vanguard) through thick and thin, and currently manages muni and other fixed income SMA strategies for City Different Investments, I don’t think it’s time for investors to abandon fixed income.

First, over the long term, diversifying a portfolio by including both stocks and bonds can help reduce risk. And in the short run, there are 4 steps you take to help you feel better about the prospect of rising inflation.

- Don’t panic. In periods of volatility—when interest rates bounce up and down—we sometimes see investors move en masse into and out of markets. Panicked buying and selling are rarely recipes for success. Step back. Make sure you have in place an investment plan that considers not only your objectives, but also an honest evaluation of your tolerance for risk. How much variation in the value of your investments can you psychologically tolerate? Do not stretch for yield, and do not let the allure of extra income induce you to overpay, or otherwise influence your investment plan. If you feel comfortable with your investments only when everything is going your way, then you’re in the wrong portfolio.

- Stay short on the yield curve. Right now, longer-term securities simply aren’t paying investors enough extra yield to compensate for the extra volatility they bring. They’re not worth the risk. In our view, the 1-5 year range of both the Treasury and municipal markets provide the best tradeoff between risk and income.

- Be confident in your investment horizon. Reexamine your horizon and make sure you really have the time it takes to ride out market volatility. A 1-5-year laddered allocation to either the Treasury or municipal market would have a duration of about 2.5 years. A rate increase would cause an initial drop in Net Asset Value (NAV), the value of the portfolio. But over the next 2.5 years, that capital loss would be recovered as the securities in the portfolio mature and those proceeds would be invested at higher rates, thus improving the investors’ dividend.

- If you’re in munis, focus on more than taxes. Taxes may yet rise, and that will impact valuations in the municipal market. But as of this writing, the amount and timing of the increases are still unknown. In our opinion, the short end (1-5 years maturity range) of the fixed income markets currently provides the best tradeoffs between income (low) and risk (still lower than longer maturity ranges).

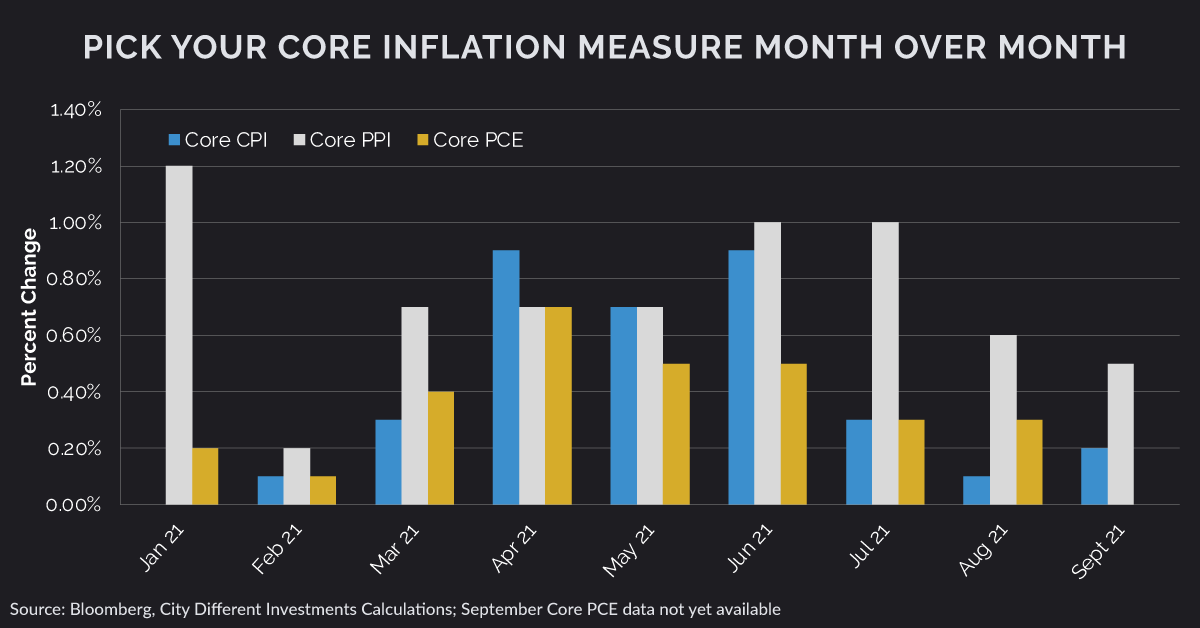

No one can ever be certain what the future will bring, but prognostication is particularly problematic right now. For the past year, I’ve been asking myself how strong the case for inflation really is. Certainly, the pandemic stifled economic activity around the globe, an effect that is quite the opposite of inflationary. However, we believe the pandemic and reactions to it set the stage for future inflationary pressures, and we are now witnessing the results.

In the meanwhile, the 4 steps I’ve outlined above seem like sensible ways to prepare a portfolio for a new price environment without making any panicked moves. At the very least, they will encourage you to reexamine some of the assumptions and expectations you have built into your portfolios, and whether you think they still hold up in this new world of ours.