.png)

U.S. homeowners are facing the dual challenges of more frequent weather events as well as disappearing property insurance. One company has been steadfast in insuring coastal properties in Florida for the past 15 years.

[Tropical storm Hillary in California in 2023. Source: Pensacola News Journal ]

Faced with the rising frequency of extreme weather, private insurance companies have increasingly quit or reduced coverage, concluding that the risks posed by climate change outweigh the potential profits. This has been most acute in several coastal states like California and Florida. But many other states have also seen substantial increases in the price of property insurance.

Mitigating Risks

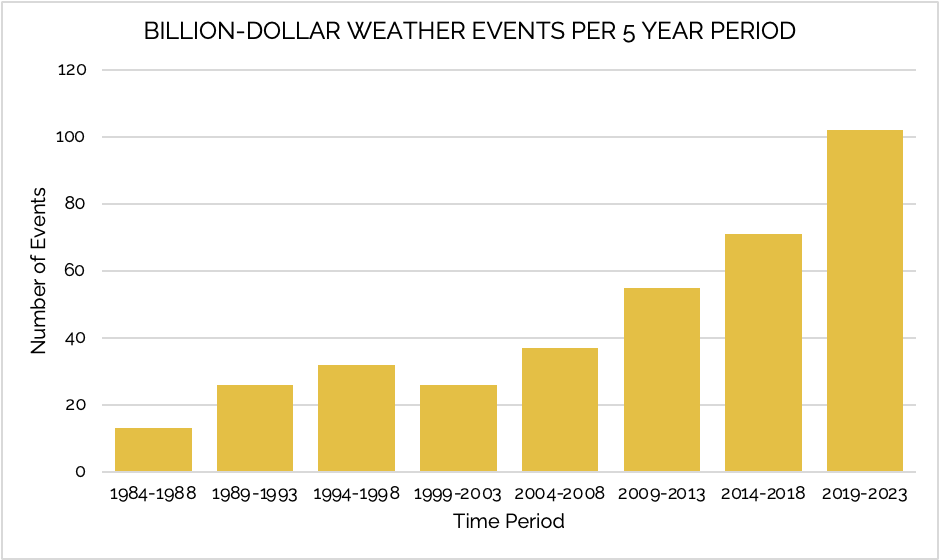

Between 1980 and 2018, the U.S. averaged 7.4 natural disasters per year, which caused >$1 billion worth of damage. But in the last five years, that number has climbed to 20.4 a year on average. Plainly, weather is playing an increasingly important role in our national economy. And while insurance does not reduce the damage caused by catastrophes, it can substantially mitigate the financial and psychological toll. It reduces the broader economic fallout by helping homeowners, businesses, and communities recover more quickly than they would otherwise.

[Source: National Centers for Environmental Information]

In addition to the increased prevalence of extreme weather events, it’s worth noting that 40% of Americans live in coastal counties, which are more vulnerable to rising sea levels (even though these counties are only 10% of U.S. land mass). In recent years, Americans have migrated towards lower-tax, more affordable states like Florida, North Carolina, and Texas, all exposed to hurricane and sea-level risks.

Impact on Insurance Industry

Because of these trends, the property insurance industry has faced rapid growth in claims and has lost money in five of the past six years. Industry leader Allstate lost over $1 billion in 2022 and then lost $2.7 billion in the second quarter of 2023 alone — more than twice that of the same period in 2022 (Travelers Insurance also doubled its catastrophe losses to $1.5 billion in the same quarter). Insurers have also grappled with supply chain issues (which have increased costs to repair damages) and political resistance when trying to raise rates in certain markets.

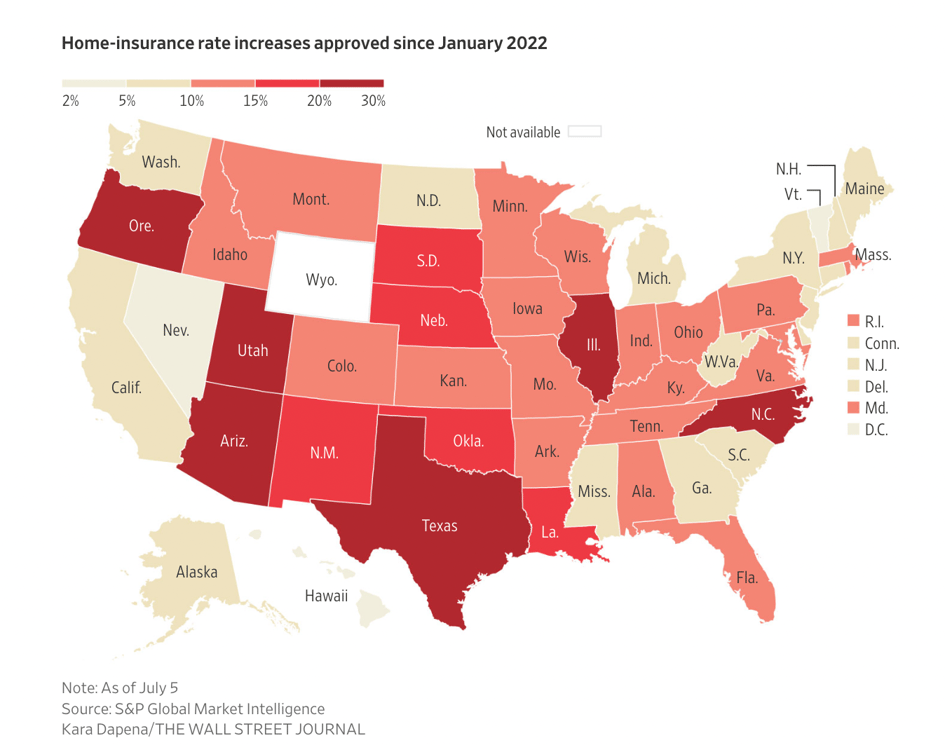

Nevertheless, between January 2022 and July 2023, there were double-digit home insurance rate increases in 31 states. Arizona, Texas, North Carolina, Oregon, Illinois, and Utah enacted the largest approved rate increases, ranging from 20% to 30%. In addition to these price increases, home insurers have increased deductibles, reduced coverage levels, and tightened eligibility requirements in an attempt to reduce their losses.

Insurance companies have also increasingly relied upon reinsurance, which protects the insurers themselves against long-tailed catastrophe losses that could impair their equity. But reinsurance costs have risen too, and this is passed on to homeowners. To add another wrinkle, reinsurance is a global industry in which the economic impacts of weather events are interrelated — losses from earthquakes in Japan can affect reinsurance pricing for hurricanes in the U.S., and in fact, reinsurance costs have gone up 30-50% this year in Florida, partly based upon global weather events of the past few years.

American Coastal Insurance (ACIC)

American Coastal Insurance Corp. (Nasdaq: ACIC) insures commercial residential properties–e.g. garden style condominiums–and has the number one market share in this segment in Florida (with roughly 4,500 policies and $637 million of premiums in force). Founded by CEO and 30%-owner Daniel Peet in 2007, ACIC now has ~35% market share of its target market. Prior to starting American Coastal, Mr. Peet founded AmRisc, a managing general insurance agent (MGA) that provides analytical and underwriting support services (without underwriting risk) for commercial property insurers. AmRisc itself has been very successful and is today a subsidiary of Truist Securities, servicing more than $2 billion in annual gross premiums.

American Coastal’s CEO observed many insurance carriers leaving the Florida market after a string of major hurricane losses in 2004 and 2005. So he founded ACIC and focused specifically on insuring garden-style condominiums, which are typically 1-4 stories tall and have a homeowners’ association. While this segment has better-than-average risk characteristics due to both the nature of the buildings insured (brick or concrete) and their locations (farther from the coast), it was neglected by the major carriers that chose instead to focus on high-rise properties with larger premiums.

American Coastal originally grew within Truist Securities, leveraging AmRisc as American Coastal’s managing general agent. Under a longstanding partnership between the two entities, American Coastal today gets a first look at prospective policies and is able to use AmRisc’s underwriting support services to price appropriately. This, in concert with its niche market focus and other factors–has rendered American Coastal Insurance profitable every year since its creation, including the years when hurricanes Irma, Michael, and Ian hit Florida.

Valuation and Risks

American Coastal shares have stormed back from distressed levels over the past year, and have already been a large contributor to our global equity strategies. But over the coming year, as ACIC continues to operate profitably, we expect the company to retain more underwriting risk and reduce its costs of reinsurance. The company may also show progress in developing its nascent capital-light MGA servicing business as a separate subsidiary. So, if we squint a little, we believe it is possible to see earnings per share of roughly $2 coming into view in the next couple of years. In that scenario, ACIC’s current share price of $11.50 (as of 01/19/2024) equates to about 5.7x EPS.

There are risks in every investment. In the case of ACIC, the company pays no dividends and operates in a heavily regulated and politicized industry. And, of course, unpredictable weather events and claims will continue to be a substantial cost for the company. However, we are encouraged by the experience and incentives of management, as well as American Coastal’s long record of profitability.

IMPORTANT DISCLOSURES

This post is for informational purposes only and should not be viewed as a recommendation to buy or sell any security or personalized investment advice. The information and statistics contained herein have been obtained from sources we believe to be reliable but cannot be guaranteed. Any projections, market outlooks, or estimates are forward-looking statements and are based upon certain assumptions. Other events that were not taken into account may occur and may significantly affect the returns or performance of these investments. Any projections, outlooks, or assumptions are subject to change without notice, and should not be construed to be indicative of the actual events which will occur. Past performance is not indicative of future results. There can be no guarantee that any strategy will be successful. All investing involves risk, including the potential loss of principal. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. No discussion or information contained herein serves as the provision of, or as a substitute for, personalized investment advice. To the extent that a reader has any questions regarding the applicability above to his/her individual situation of any specific issue discussed, he/she is encouraged to consult with the professional advisor of his/her choosing. City Different Investments is neither a law firm nor a certified public accounting firm, and no portion of this content should be construed as legal, tax, or accounting advice.